UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): May 1, 2014

XPO LOGISTICS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 001-32172 | 03-0450326 | ||

| (State or other jurisdiction of incorporation) |

(Commission File Number) |

(I.R.S. Employer Identification No.) |

Five Greenwich Office Park, Greenwich, Connecticut 06831

(Address of principal executive offices)

(855) 976-4636

(Registrant’s telephone number, including area code)

N/A

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

| Item 2.02. | Results of Operations and Financial Condition |

On May 1, 2014, XPO Logistics, Inc. (the “Company”) issued a press release announcing its results of operations for the fiscal quarter ended March 31, 2014. A copy of the press release is furnished as Exhibit 99.1 to this Current Report on Form 8-K.

The information furnished pursuant to this Item 2.02, including Exhibit 99.1, shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities under that Section and shall not be deemed to be incorporated by reference into any filing of the Company under the Exchange Act or the Securities Act of 1933, as amended (the “Securities Act”), except to the extend that the registrant specifically incorporates any such information by reference.

| Item 7.01. | Regulation FD Disclosure. |

On May 1, 2014, the Company released a slide presentation expected to be used by the Company in connection with certain future investor presentations, together with a corresponding script. Copies of the slide presentation and script are attached as Exhibit 99.2 and Exhibit 99.3, respectively, to this Current Report on Form 8-K.

The slide presentation and script should be read together and with the Company’s filings with the Securities and Exchange Commission (the “SEC”), including the Quarterly Report on Form 10-Q for the quarter ended March 31, 2014.

The information furnished in this Item 7.01, including Exhibit 99.2 and Exhibit 99.3, shall not be deemed “filed” for purposes of Section 18 of the Exchange Act or otherwise subject to the liabilities of that Section, and shall not be deemed to be incorporated by reference into any filing of the Company under the Exchange Act or the Securities Act, except to the extent that the registrant specifically incorporates any such information by reference.

| Item 9.01. | Financial Statements and Exhibits. |

(d) Exhibits

| Exhibit |

Exhibit Description | |

| 99.1 | Press Release, dated May 1, 2014, issued by XPO Logistics, Inc. | |

| 99.2 | Investor Presentation, dated May 1, 2014 | |

| 99.3 | Investor Presentation Script, dated May 1, 2014 | |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Date: May 1, 2014 | XPO LOGISTICS, INC. | |||||

| By: | /s/ Gordon E. Devens | |||||

| Gordon E. Devens | ||||||

| Senior Vice President and General Counsel | ||||||

EXHIBIT INDEX

| Exhibit |

Exhibit Description | |

| 99.1 | Press Release, dated May 1, 2014, issued by XPO Logistics, Inc. | |

| 99.2 | Investor Presentation, dated May 1, 2014 | |

| 99.3 | Investor Presentation Script, dated May 1, 2014 | |

Exhibit 99.1

XPO Logistics Announces First Quarter 2014 Results

Reports 51% organic growth company-wide

Raises estimate for cost synergies from Pacer integration to $15 million

Opens freight brokerage cold-start in Kansas City

Reaffirms full year 2014 guidance

GREENWICH, Conn. — May 1, 2014 — XPO Logistics, Inc. (NYSE: XPO) today announced financial results for the first quarter of 2014. Total gross revenue increased 147.7% year-over-year to $282.4 million. Net revenue increased 259.1% to $58.4 million.1

The company reported a net loss of $28.1 million for the quarter, compared with a net loss of $14.5 million for the same period in 2013. The net loss available to common shareholders was $28.9 million, or a loss of $0.70 per diluted share, compared with a net loss of $15.3 million, or a loss of $0.85 per diluted share, for the same period in 2013. The company’s first quarter 2014 results reflect: $10.8 million, or $7.5 million after-tax, of transaction and integration costs related to the acquisition of Pacer International, Inc.; $4.5 million, or $3.7 million after-tax, for a commitment fee related to an undrawn debt funding option for the Pacer transaction; and $2.3 million, before-tax and after-tax, related to conversions of the company’s convertible senior notes.

Earnings (loss) before interest, taxes, depreciation and amortization (“EBITDA”), a non-GAAP financial measure, was a loss of $10.1 million for the quarter, compared with a loss of $9.8 million for the same period in 2013. EBITDA for the first quarter reflects $1.4 million and $1.1 million of non-cash share-based compensation for 2014 and 2013, respectively. Excluding $10.8 million of transaction and integration costs related to the Pacer acquisition, adjusted EBITDA for the first quarter of 2014 was $678,000. Reconciliations of EBITDA and adjusted EBITDA to net income are provided in the attached financial tables.

The company had approximately $157 million of cash, including $13 million of restricted cash, as of March 31, 2014, immediately following its acquisition of Pacer.

Reaffirms Full Year Financial Targets

The company reaffirmed its full year 2014 targets for an annual revenue run rate of at least $2.75 billion and an annual EBITDA run rate of at least $100 million by December 31. The company expects to acquire at least $400 million of historical annual revenue in 2014, excluding the Pacer acquisition.

| 1 | Effective 2014, the company began reporting Net Revenue and Net Revenue Margin instead of the equivalent Gross Margin and Gross Margin Percentage to conform the presentation of operating expenses with its acquired intermodal operations. Refer to the attached financial tables for further information. |

CEO Comments

Bradley Jacobs, chairman and chief executive officer of XPO Logistics, said, “In the first quarter, we increased our revenue to $282 million – significantly more than expected – including notable year-over-year organic growth of 51%. Our 11 brokerage cold-starts, including our newest branch in Kansas City, are on a combined revenue run rate of $190 million, nearly triple the rate of 12 months ago. Our employee productivity metrics are on the rise, and our strategic accounts team signed 33 new major accounts in the quarter.

“Our expedited business, which benefited from weather-related supply chain disruptions, increased first quarter profitability fivefold from a year ago. This included the impact of our online portal XPO NLM, which we purchased in December: XPO NLM managed over 130,000 expedited loads in the first quarter, a 47% increase in volume from a year ago. We increased freight forwarding revenue by more than 20% year-over-year, and improved our brokerage margin by 90 basis points, excluding the benefit of last-mile margin. We capped the quarter with our purchase of Pacer International on March 31.

“The integration of Pacer is going extremely well. We’ve already unified our sales force, and we have many large intermodal bids in the pipeline. We moved the former Pacer truck brokerage operation onto our proprietary Freight Optimizer technology, giving them access to our network of over 26,000 carriers. And we’ve made great progress at right-sizing costs in technology, real estate, sales and administrative functions. We acted quickly to reverse the losses in Pacer’s logistics business by closing 10 underperforming locations and consolidating six duplicative offices in the U.S., Asia and Europe. The remaining locations have become part of our XPO Global Logistics freight forwarding network. We now expect to capture about $15 million of cost synergies – three times our original estimate – while expanding services to our customers.”

Jacobs continued, “Excluding the costs associated with the acquisition of Pacer, this was our second straight quarter of positive EBITDA. We’re on track to meet our target run rate of $100 million of EBITDA by year-end 2014, and approximately $425 million of EBITDA in 2017 on revenue of $7.5 billion.”

First Quarter 2014 Results by Business Unit

| • | Freight brokerage: The company’s freight brokerage business generated total gross revenue of $231.7 million for the quarter, a 196.2% increase from the same period in 2013. Net revenue margin1 was 19.1%, compared with 12.9% in 2013, an improvement of 620 basis points. The year-over-year increases in revenue and margin for the quarter were primarily due to the acquisition of high-margin last-mile logistics providers 3PD and Optima Service Solutions in 2013, 75% organic revenue growth, and continued margin improvement. Excluding the benefit of last-mile margin, freight brokerage net revenue margin improved 90 basis points, compared with 2013. The increase in net revenue was offset by higher intangible asset amortization related to acquisitions, and by the company’s strategic investments in sales and procurement personnel over the trailing 12 months. First quarter operating income was a loss of $4.0 million, compared with a loss of $3.8 million a year ago. |

| • | Expedited transportation: The company’s expedited transportation business generated total gross revenue of $33.8 million for the quarter, a 41.6% increase from the same period in 2013. Net revenue margin was 33.6%, compared with 15.9% in 2013, an improvement of 1,770 basis points. The year-over-year increase in net revenue margin primarily reflects |

| the acquisition of managed transportation expeditor NLM, which generated $6.4 million of gross revenue and net revenue in the first quarter. Excluding NLM, expedited net revenue margin improved, driven largely by higher revenue per mile. First quarter operating income was $3.7 million, compared with $753,000 a year ago, primarily reflecting the positive impact of NLM and significant organic margin improvement. |

| • | Freight forwarding: The company’s freight forwarding business generated total gross revenue of $19.5 million for the quarter, a 20.2% increase from the same period in 2013. Net revenue margin was 13.9%, compared with 14.7% in 2013. The decrease in net revenue margin was primarily due to an increase in international shipments, which typically generate higher revenue, but at a lower margin, than domestic shipments. First quarter operating income was $552,000, a 48.4% increase year-over-year. |

| • | Corporate: Corporate SG&A expense for the first quarter of 2014 was $21.7 million, compared with $8.7 million for the first quarter of 2013. Corporate SG&A includes: $6.4 million, or $5.3 million after-tax, of integration charges related to the acquisition of Pacer; $4.6 million, or $4.1 million after-tax, of acquisition-related transaction costs primarily related to Pacer; and $1.2 million, or $1.0 million after-tax, of litigation costs. |

Raises Estimate for Cost Synergies from Pacer Integration to $15 Million

The company increased its target for cost synergies related to the integration of Pacer International, Inc., acquired March 31, 2014. The company now expects to realize approximately $15 million of synergies.

Opens Freight Brokerage Cold-start in Kansas City

On March 31, 2014, the company opened a cold-start location in Kansas City, Mo., as part of a planned organic expansion of its freight brokerage footprint. The branch is the company’s eleventh freight brokerage cold-start.

Conference Call

The company will hold a conference call on Friday, May 2, 2014, at 8:30 a.m. Eastern Time. Participants can call toll-free (from U.S./Canada) 1-800-708-4539; international callers dial +1-847-619-6396. A live webcast of the conference will be available on the investor relations area of the company’s website, www.xpologistics.com/investors. The conference will be archived until June 1, 2014. To access the replay by phone, call toll-free (from U.S./Canada) 1-888-843-7419; international callers dial +1-630-652-3042. Use participant passcode 37094021.

About XPO Logistics, Inc.

XPO Logistics, Inc. (NYSE: XPO) is one of the fastest growing providers of transportation logistics services in North America: the fourth largest freight brokerage firm, the third largest provider of intermodal services, the largest provider of last-mile logistics for heavy goods, and the largest manager of expedited shipments, with growing positions in managed transportation, global freight forwarding and less-than-truckload brokerage. The company facilitates more than 25,000 deliveries a day throughout the U.S., Mexico and Canada.

XPO Logistics has 123 locations and approximately 3,000 employees. Its three business segments – freight brokerage, expedited transportation and freight forwarding – utilize

relationships with ground, rail, sea and air carriers to serve over 14,000 customers in the manufacturing, industrial, retail, commercial, life sciences and government sectors. The company has more than 1,000 owner-operator trucks under contract to its drayage and expedited subsidiaries, and has access to additional capacity through its relationships with over 26,000 other carriers. For more information: www.xpologistics.com

Explanatory Note Regarding Impact of Pacer Acquisition

The company acquired Pacer International, Inc. on March 31, 2014. Accordingly, the company’s financial statements for the first quarter of 2014 do not include any results of operations for Pacer. However, the balance sheet for Pacer is reflected in the company’s consolidated balance sheets as of March 31.

Non-GAAP Financial Measures

This press release contains certain non-GAAP financial measures as defined under Securities and Exchange Commission (“SEC”) rules, such as earnings (loss) before interest, taxes, depreciation and amortization (“EBITDA”) and adjusted EBITDA for the quarters ended March 31, 2014 and 2013. As required by SEC rules, we provide reconciliations of these measures to the most directly comparable measure under United States generally accepted accounting principles (“GAAP”), which are set forth in the attachments to this release. We believe that EBITDA and adjusted EBITDA improve comparability from period to period by removing the impact of our capital structure (interest expense from our outstanding debt), asset base (depreciation and amortization) and tax consequences, and, in the case of adjusted EBITDA, non-recurring costs related to the Pacer acquisition. In addition to its use by management, we believe that EBITDA and adjusted EBITDA are measures widely used by securities analysts, investors and others to evaluate the financial performance of companies in our industry. Other companies may calculate EBITDA and adjusted EBITDA differently, and therefore our measures may not be comparable to similarly titled measures of other companies. EBITDA and adjusted EBITDA are not measures of financial performance or liquidity under GAAP and should not be considered in isolation or as an alternative to net income, cash flows from operating activities and other measures determined in accordance with GAAP. Items excluded from EBITDA and adjusted EBITDA are significant and necessary components of the operations of our business, and, therefore, EBITDA and adjusted EBITDA should only be used as supplemental measures of our operating performance.

Forward-looking Statements

This press release includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, including the company’s full year 2014 and full year 2017 financial targets and expected cost synergies from the Pacer integration. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. In some cases, forward-looking statements can be identified by the use of forward-looking terms such as “anticipate,” “estimate,” “believe,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict,” “should,” “will,” “expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target” or the negative of these terms or other comparable terms. However, the absence of these words does not mean that the statements are not forward-looking. These forward-looking statements are based on certain assumptions and analyses made by us in light of our experience and our perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate in the circumstances.

These forward-looking statements are subject to known and unknown risks, uncertainties and assumptions that may cause actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. Factors that might cause or contribute to a material difference include, but are not limited to, those discussed in XPO’s filings with the SEC and the following: economic conditions generally; competition; XPO’s ability to find suitable acquisition candidates and execute its acquisition strategy; the expected impact of acquisitions, including the expected impact on XPO’s results of operations; XPO’s ability to raise debt and equity capital; XPO’s ability to attract and retain key employees to execute its growth strategy; litigation, including litigation related to alleged misclassification of independent contractors; the ability to develop and implement a suitable information technology system; the ability to maintain positive relationships with XPO’s networks of third-party transportation providers; the ability to retain XPO’s and acquired businesses’ largest customers; XPO’s ability to successfully integrate acquired businesses and realize anticipated synergies and cost savings; rail and other network changes; weather and other service disruptions; and governmental regulation. All forward-looking statements set forth in this press release are qualified by these cautionary statements and there can be no assurance that the actual results or developments anticipated will be realized or, even if substantially realized, that they will have the expected consequences to, or effects on, XPO or its businesses or operations. Forward-looking statements set forth in this document speak only as of the date hereof, and XPO undertakes no obligation to update forward-looking statements to reflect subsequent events or circumstances, changes in expectations or the occurrence of unanticipated events except to the extent required by law.

Investor Contact:

XPO Logistics, Inc.

Tavio Headley, +1-203-930-1602

tavio.headley@xpologistics.com

Media Contacts:

Brunswick Group

Gemma Hart, Darren McDermott, +1-212-333-3810

XPO Logistics, Inc.

Condensed Consolidated Statements of Operations

(Unaudited)

(In thousands, except per share data)

| Three Months Ended March 31, |

||||||||

| 2014 | 2013 | |||||||

| Revenue |

$ | 282,403 | $ | 113,999 | ||||

| Operating expenses |

||||||||

| Cost of purchased transportation and services |

224,006 | 97,739 | ||||||

| Direct operating expense |

3,880 | — | ||||||

| Sales, general and administrative expense |

75,878 | 27,627 | ||||||

|

|

|

|

|

|||||

| Total operating expenses |

303,764 | 125,366 | ||||||

|

|

|

|

|

|||||

| Operating loss |

(21,361 | ) | (11,367 | ) | ||||

|

|

|

|

|

|||||

| Other expense (income) |

15 | (109 | ) | |||||

| Interest expense |

10,058 | 3,064 | ||||||

|

|

|

|

|

|||||

| Loss before income tax provision |

(31,434 | ) | (14,322 | ) | ||||

| Income tax (benefit) provision |

(3,299 | ) | 222 | |||||

|

|

|

|

|

|||||

| Net loss |

(28,135 | ) | (14,544 | ) | ||||

| Cumulative preferred dividends |

(742 | ) | (743 | ) | ||||

|

|

|

|

|

|||||

| Net loss available to common shareholders |

$ | (28,877 | ) | $ | (15,287 | ) | ||

|

|

|

|

|

|||||

| Basic loss per share |

||||||||

| Net loss |

$ | (0.70 | ) | $ | (0.85 | ) | ||

| Diluted loss per share |

||||||||

| Net loss |

$ | (0.70 | ) | $ | (0.85 | ) | ||

| Weighted average common shares outstanding |

||||||||

| Basic weighted average common shares outstanding |

41,313 | 18,032 | ||||||

| Diluted weighted average common shares outstanding |

41,313 | 18,032 | ||||||

XPO Logistics, Inc.

Condensed Consolidated Balance Sheets

(In thousands, except share data)

| March 31, 2014 |

December 31, 2013 |

|||||||

| (Unaudited) | ||||||||

| ASSETS | ||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 143,886 | $ | 21,524 | ||||

| Accounts receivable, net of allowances of $5,066 and $3,539, respectively |

342,752 | 134,227 | ||||||

| Prepaid expenses |

8,515 | 3,935 | ||||||

| Deferred tax asset, current |

6,182 | 3,041 | ||||||

| Other current assets |

10,869 | 7,304 | ||||||

|

|

|

|

|

|||||

| Total current assets |

512,204 | 170,031 | ||||||

|

|

|

|

|

|||||

| Property and equipment, net of $15,658 and $11,803 in accumulated depreciation, respectively |

98,819 | 56,571 | ||||||

| Goodwill |

539,168 | 363,448 | ||||||

| Identifiable intangible assets, net of $22,722 and $15,411 in accumulated amortization, respectively |

250,203 | 185,179 | ||||||

| Deferred tax asset, long-term |

511 | 72 | ||||||

| Restricted cash |

13,332 | 2,141 | ||||||

| Other long-term assets |

9,518 | 2,799 | ||||||

|

|

|

|

|

|||||

| Total long-term assets |

911,551 | 610,210 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 1,423,755 | $ | 780,241 | ||||

|

|

|

|

|

|||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: |

||||||||

| Accounts payable |

$ | 227,738 | $ | 71,391 | ||||

| Accrued salaries and wages |

19,257 | 11,741 | ||||||

| Accrued expenses, other |

45,947 | 9,489 | ||||||

| Current maturities of long-term debt |

1,777 | 2,028 | ||||||

| Other current liabilities |

6,486 | 4,684 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

301,205 | 99,333 | ||||||

|

|

|

|

|

|||||

| Convertible senior notes |

99,844 | 106,268 | ||||||

| Revolving credit facility and other long-term debt, net of current maturities |

470 | 75,373 | ||||||

| Deferred tax liability, long-term |

24,793 | 15,200 | ||||||

| Other long-term liabilities |

32,663 | 28,224 | ||||||

|

|

|

|

|

|||||

| Total long-term liabilities |

157,770 | 225,065 | ||||||

|

|

|

|

|

|||||

| Commitments and contingencies |

||||||||

| Stockholders’ equity: |

||||||||

| Preferred stock, $.001 par value; 10,000,000 shares; 73,335 and 74,175 shares issued and outstanding, respectively |

42,258 | 42,737 | ||||||

| Common stock, $.001 par value; 150,000,000 shares authorized; 52,570,800 and 30,583,073 shares issued, respectively; and 52,525,800 and 30,538,073 shares outstanding, respectively |

53 | 30 | ||||||

| Additional paid-in capital |

1,063,242 | 524,972 | ||||||

| Treasury stock, at cost, 45,000 shares held |

(107 | ) | (107 | ) | ||||

| Accumulated deficit |

(140,666 | ) | (111,789 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

964,780 | 455,843 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 1,423,755 | $ | 780,241 | ||||

|

|

|

|

|

|||||

XPO Logistics, Inc.

Condensed Consolidated Statements of Cash Flows

(Unaudited)

(In thousands)

| Three Months Ended March 31, |

||||||||

| 2014 | 2013 | |||||||

| Operating activities |

||||||||

| Net loss |

$ | (28,135 | ) | $ | (14,544 | ) | ||

| Adjustments to reconcile net loss to net cash from operating activities |

||||||||

| Provisions for allowance for doubtful accounts |

2,196 | 231 | ||||||

| Depreciation and amortization |

11,273 | 1,554 | ||||||

| Stock compensation expense |

2,206 | 1,097 | ||||||

| Accretion of debt |

1,430 | 1,438 | ||||||

| Other |

2,062 | (211 | ) | |||||

| Changes in assets and liabilities, net of effects of acquisitions: |

||||||||

| Accounts receivable |

(56,414 | ) | (9,771 | ) | ||||

| Deferred tax expense |

(4,529 | ) | 135 | |||||

| Income tax payable |

2,298 | (814 | ) | |||||

| Prepaid expense and other current assets |

114 | (62 | ) | |||||

| Other long-term assets |

(96 | ) | (2 | ) | ||||

| Accounts payable |

48,676 | (3,417 | ) | |||||

| Accrued expenses and other liabilities |

10,177 | (3,659 | ) | |||||

|

|

|

|

|

|||||

| Cash flows used by operating activities |

(8,742 | ) | (28,025 | ) | ||||

|

|

|

|

|

|||||

| Investing activities |

||||||||

| Acquisition of businesses, net of cash acquired |

(190,962 | ) | (16,560 | ) | ||||

| Payment for purchases of property and equipment |

(3,935 | ) | (1,081 | ) | ||||

| Other |

246 | 125 | ||||||

|

|

|

|

|

|||||

| Cash flows used by investing activities |

(194,651 | ) | (17,516 | ) | ||||

|

|

|

|

|

|||||

| Financing activities |

||||||||

| Repayment of borrowings on revolving debt facility |

(75,000 | ) | — | |||||

| Proceeds from stock offering, net |

413,183 | — | ||||||

| Payment for cash held as collateral in lending arrangement |

(11,269 | ) | — | |||||

| Dividends paid to preferred stockholders |

(742 | ) | (743 | ) | ||||

| Other |

(417 | ) | 173 | |||||

|

|

|

|

|

|||||

| Cash flows provided (used) by financing activities |

325,755 | (570 | ) | |||||

|

|

|

|

|

|||||

| Net increase (decrease) in cash |

122,362 | (46,111 | ) | |||||

| Cash and cash equivalents, beginning of period |

21,524 | 252,293 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents, end of period |

$ | 143,886 | $ | 206,182 | ||||

|

|

|

|

|

|||||

| Supplemental disclosure of cash flow information: |

||||||||

| Cash paid for interest |

$ | 4,287 | $ | 3,328 | ||||

| Cash (received) paid for income taxes |

$ | (1,507 | ) | $ | 732 | |||

| Equity portion of acquisition purchase price |

$ | 108,815 | $ | 2,573 | ||||

Freight Brokerage

Summary Financial Table

(Unaudited)

(In thousands)

| Three Months Ended March 31, | ||||||||||||||||

| 2014 | 2013 | $ Variance | Change % | |||||||||||||

| Revenue |

$ | 231,689 | $ | 78,230 | $ | 153,459 | 196.2 | % | ||||||||

| Cost of purchased transportation and services |

187,372 | 68,164 | 119,208 | 174.9 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net revenue |

44,317 | 10,066 | 34,251 | 340.3 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Direct operating expense |

3,880 | — | 3,880 | 100.0 | % | |||||||||||

| SG&A expense |

||||||||||||||||

| Salaries & benefits |

25,526 | 10,163 | 15,363 | 151.2 | % | |||||||||||

| Other SG&A expense |

7,841 | 1,895 | 5,946 | 313.8 | % | |||||||||||

| Purchased services |

2,072 | 814 | 1,258 | 154.5 | % | |||||||||||

| Depreciation & amortization |

8,993 | 1,014 | 7,979 | 786.9 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total SG&A expense |

44,432 | 13,886 | 30,546 | 220.0 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating loss |

$ | (3,995 | ) | $ | (3,820 | ) | $ | (175 | ) | 4.6 | % | |||||

|

|

|

|

|

|

|

|

|

|||||||||

Freight Brokerage

Key Data

(In thousands, except personnel data)

| 3 Mos Ended March 31, 2014 |

3 Mos Ended March 31, 2013 |

|||||||

| Revenue |

||||||||

| Truckload, LTL, and Intermodal |

$ | 144,585 | $ | 78,230 | ||||

| Last Mile |

87,104 | — | ||||||

|

|

|

|

|

|||||

| Total Revenue |

$ | 231,689 | $ | 78,230 | ||||

|

|

|

|

|

|||||

| Net Revenue |

||||||||

| Truckload, LTL, and Intermodal |

$ | 19,921 | $ | 10,066 | ||||

| Last Mile |

24,396 | — | ||||||

|

|

|

|

|

|||||

| Total Net Revenue |

$ | 44,317 | $ | 10,066 | ||||

|

|

|

|

|

|||||

| Net Revenue % |

||||||||

| Truckload, LTL, and Intermodal |

13.8 | % | 12.9 | % | ||||

| Last Mile |

28.0 | % | — | |||||

|

|

|

|

|

|||||

| Overall Net Revenue % |

19.1 | % | 12.9 | % | ||||

|

|

|

|

|

|||||

| Freight Brokerage personnel (end of period) |

2,331 | 668 | ||||||

Note: Employee totals are as of period end, and primarily include the positions of shipper sales, carrier procurement and brokerage operations, and reflect the impact of recruitment and acquisitions.

Expedited Transportation

Summary Financial Table

(Unaudited)

(In thousands)

| Three Months Ended March 31, | ||||||||||||||||

| 2014 | 2013 | $ Variance | Change % | |||||||||||||

| Revenue |

$ | 33,810 | $ | 23,875 | $ | 9,935 | 41.6 | % | ||||||||

| Cost of purchased transportation and services |

22,442 | 20,067 | 2,375 | 11.8 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net revenue |

11,368 | 3,808 | 7,560 | 198.5 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| SG&A expense |

||||||||||||||||

| Salaries & benefits |

4,154 | 1,945 | 2,209 | 113.6 | % | |||||||||||

| Other SG&A expense |

1,456 | 604 | 852 | 141.1 | % | |||||||||||

| Purchased services |

434 | 289 | 145 | 50.2 | % | |||||||||||

| Depreciation & amortization |

1,578 | 217 | 1,361 | 627.2 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total SG&A expense |

7,622 | 3,055 | 4,567 | 149.5 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income |

$ | 3,746 | $ | 753 | $ | 2,993 | 397.5 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Note: Total depreciation and amortization for the Expedited Transportation reportable segment included in both direct expense and SG&A, was $1,612,000 and $268,000 for the three-months ended March 31, 2014 and 2013, respectively.

Freight Forwarding

Summary Financial Table

(Unaudited)

(In thousands)

| Three Months Ended March 31, | ||||||||||||||||

| 2014 | 2013 | $ Variance | Change % | |||||||||||||

| Revenue |

$ | 19,506 | $ | 16,233 | $ | 3,273 | 20.2 | % | ||||||||

| Cost of purchased transportation and services |

16,793 | 13,847 | 2,946 | 21.3 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net revenue |

2,713 | 2,386 | 327 | 13.7 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| SG&A expense |

||||||||||||||||

| Salaries & benefits |

1,635 | 1,433 | 202 | 14.1 | % | |||||||||||

| Other SG&A expense |

349 | 403 | (54 | ) | -13.4 | % | ||||||||||

| Purchased services |

77 | 90 | (13 | ) | -14.4 | % | ||||||||||

| Depreciation & amortization |

100 | 88 | 12 | 13.6 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total SG&A expense |

2,161 | 2,014 | 147 | 7.3 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income |

$ | 552 | $ | 372 | $ | 180 | 48.4 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

XPO Corporate

Summary of Sales, General & Administrative Expense

(Unaudited)

(In thousands)

| Three Months Ended March 31, | ||||||||||||||||

| 2014 | 2013 | $ Variance | Change % | |||||||||||||

| SG&A expense |

||||||||||||||||

| Salaries & benefits |

$ | 9,844 | $ | 4,507 | $ | 5,337 | 118.4 | % | ||||||||

| Other SG&A expense |

3,620 | 1,359 | 2,261 | 166.4 | % | |||||||||||

| Purchased services |

7,632 | 2,622 | 5,010 | 191.1 | % | |||||||||||

| Depreciation & amortization |

568 | 184 | 384 | 208.7 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total SG&A expense |

$ | 21,664 | $ | 8,672 | $ | 12,992 | 149.8 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Note: Intercompany eliminations included revenue of $2.6 million and $4.3 million for the three-months ended March 31, 2014 and 2013, respectively.

Reconciliation of Non-GAAP Measures

XPO Logistics, Inc.

Consolidated Reconciliation of EBITDA to Net Loss

(In thousands)

| Three Months Ended March 31, |

||||||||||||

| 2014 | 2013 | Change % | ||||||||||

| Net loss available to common shareholders |

$ | (28,877 | ) | $ | (15,287 | ) | 88.9 | % | ||||

| Preferred dividends |

(742 | ) | (743 | ) | -0.1 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Net loss |

(28,135 | ) | (14,544 | ) | 93.4 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Interest expense |

10,058 | 3,064 | 228.3 | % | ||||||||

| Income tax benefit |

(3,299 | ) | 222 | -1586.0 | % | |||||||

| Depreciation and amortization |

11,273 | 1,502 | 650.5 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| EBITDA |

$ | (10,103 | ) | $ | (9,756 | ) | 3.6 | % | ||||

|

|

|

|

|

|

|

|||||||

| Pacer transaction and restructuring costs |

(10,781 | ) | — | 100.0 | % | |||||||

|

|

|

|

|

|

|

|||||||

| Adjusted EBITDA |

$ | 678 | $ | (9,756 | ) | -106.9 | % | |||||

|

|

|

|

|

|

|

|||||||

Note: Please refer to the “Non-GAAP Financial Measures” section of the press release.

XPO Logistics, Inc.

Consolidated Calculation of Diluted Weighted Shares Outstanding

| Three Months Ended | ||||||||

| March 31, 2014 | March 31, 2013 | |||||||

| Basic common stock outstanding |

41,312,894 | 18,031,926 | ||||||

|

|

|

|

|

|||||

| Potentially Dilutive Securities: |

||||||||

| Shares underlying the conversion of preferred stock to common stock |

10,503,286 | 10,610,714 | ||||||

| Shares underlying the conversion of the convertible senior notes |

7,741,643 | 8,749,239 | ||||||

| Shares underlying warrants to purchase common stock |

8,004,967 | 6,342,298 | ||||||

| Shares underlying stock options to purchase common stock |

529,385 | 550,611 | ||||||

| Shares underlying restricted stock units |

565,825 | 414,088 | ||||||

|

|

|

|

|

|||||

| 27,345,106 | 26,666,950 | |||||||

|

|

|

|

|

|||||

|

|

|

|

|

|||||

| Diluted weighted shares outstanding |

68,658,000 | 44,698,876 | ||||||

|

|

|

|

|

|||||

Note: For dilution purposes, GAAP requires diluted shares to be reflected on a weighted average basis, which takes into account the portion of the period in which the diluted shares were outstanding. The table above reflects the weighted average diluted shares for the periods presented. The impact of this dilution was not reflected in the earnings per share calculations on the Condensed Consolidated Statements of Operations because the impact was anti-dilutive. The treasury method was used to determine the shares underlying the warrants to purchase common stock with an average closing market price of common stock of $28.85 per share and $17.15 per share for the three months ended March 31, 2014 and 2013, respectively.

For informational purposes, the following table represents fully diluted shares as of March 31, 2014, calculated on a non-weighted basis without giving effect to the portion of any period in which the diluted shares were outstanding. The dilutive effect of the warrants, options and RSUs in the table was calculated using the closing market price of common stock on March 31, 2014. A non-weighted basis for calculating fully diluted shares is a non-GAAP financial measure as defined under SEC rules.

XPO Logistics, Inc.

| Diluted Shares as of March 31, 2014 |

||||

| Common stock outstanding |

52,525,800 | |||

| Preferred stock |

10,476,430 | |||

| Convertible senior notes |

7,341,643 | |||

| Warrants |

8,053,888 | |||

| Outstanding stock options |

648,459 | |||

| Restricted stock units |

1,577,972 | |||

|

|

|

|||

| Total |

80,624,192 | |||

|

|

|

|||

XPO Logistics, Inc.

Prior Period Results Conformed to 2014 Presentation

Consolidated Statements of Operations

(In thousands)

| AS REPORTED | For the | For the | For the | |||||||||||||||||||||||||

| Year Ended | Three Months Ended | Year Ended | ||||||||||||||||||||||||||

| December 31, 2011 |

December 31, 2012 |

March 31, 2013 |

June 30, 2013 |

September 30, 2013 |

December 31, 2013 |

December 31, 2013 |

||||||||||||||||||||||

| Revenue |

$ | 177,076 | $ | 278,591 | $ | 113,999 | $ | 137,091 | $ | 193,982 | $ | 257,231 | $ | 702,303 | ||||||||||||||

| Direct expense |

||||||||||||||||||||||||||||

| Transportation services |

133,007 | 224,035 | 94,880 | 114,924 | 156,446 | 201,555 | 567,805 | |||||||||||||||||||||

| Station commissions |

11,098 | 9,321 | 1,708 | 1,992 | 1,706 | 1,762 | 7,168 | |||||||||||||||||||||

| Other direct expense |

3,193 | 4,409 | 1,151 | 835 | 995 | 842 | 3,823 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total direct expense |

147,298 | 237,765 | 97,739 | 117,751 | 159,147 | 204,159 | 578,796 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Gross margin |

29,778 | 40,826 | 16,260 | 19,340 | 34,835 | 53,072 | 123,507 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| SG&A expense |

||||||||||||||||||||||||||||

| Salaries & benefits |

16,338 | 39,278 | 18,048 | 20,491 | 27,065 | 35,029 | 100,633 | |||||||||||||||||||||

| Other SG&A expense |

3,937 | 11,616 | 4,262 | 5,198 | 9,521 | 10,377 | 29,358 | |||||||||||||||||||||

| Purchased services |

6,733 | 15,388 | 3,815 | 5,914 | 8,311 | 7,174 | 25,214 | |||||||||||||||||||||

| Depreciation and amortization |

1,046 | 2,508 | 1,502 | 1,752 | 8,357 | 9,016 | 20,627 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total SG&A expense |

28,054 | 68,790 | 27,627 | 33,355 | 53,254 | 61,596 | 175,832 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Operating income (loss) |

$ | 1,724 | $ | (27,964 | ) | $ | (11,367 | ) | $ | (14,015 | ) | $ | (18,419 | ) | $ | (8,524 | ) | $ | (52,325 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| AS CONFORMED | For the | For the | For the | |||||||||||||||||||||||||

| Year Ended | Three Months Ended | Year Ended | ||||||||||||||||||||||||||

| December 31, 2011 |

December 31, 2012 |

March 31, 2013 |

June 30, 2013 |

September 30, 2013 |

December 31, 2013 |

December 31, 2013 |

||||||||||||||||||||||

| Revenue |

$ | 177,076 | $ | 278,591 | $ | 113,999 | $ | 137,091 | $ | 193,982 | $ | 257,231 | $ | 702,303 | ||||||||||||||

| Cost of purchased transportation and services |

147,298 | 237,765 | 97,739 | 117,751 | 159,147 | 204,159 | 578,796 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net revenue |

29,778 | 40,826 | 16,260 | 19,340 | 34,835 | 53,072 | 123,507 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Direct operating expense |

0 | 0 | 0 | 0 | 2,077 | 4,278 | 6,355 | |||||||||||||||||||||

| SG&A expense |

||||||||||||||||||||||||||||

| Salaries & benefits |

16,338 | 39,278 | 18,048 | 20,491 | 26,948 | 34,799 | 100,286 | |||||||||||||||||||||

| Other SG&A expense |

3,937 | 11,616 | 4,262 | 5,198 | 8,067 | 7,762 | 25,289 | |||||||||||||||||||||

| Purchased services |

6,733 | 15,388 | 3,815 | 5,914 | 7,805 | 5,741 | 23,275 | |||||||||||||||||||||

| Depreciation and amortization |

1,046 | 2,508 | 1,502 | 1,752 | 8,357 | 9,016 | 20,627 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total SG&A expense |

28,054 | 68,790 | 27,627 | 33,355 | 51,177 | 57,318 | 169,477 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Operating income (loss) |

$ | 1,724 | $ | (27,964 | ) | $ | (11,367 | ) | $ | (14,015 | ) | $ | (18,419 | ) | $ | (8,524 | ) | $ | (52,325 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

XPO Logistics, Inc.

Prior Period Results Conformed to 2014 Presentation

Freight Brokerage

Statement of Operations Data

(in thousands)

| AS REPORTED | For the | For the | For the | |||||||||||||||||||||||||

| Year Ended | Three Months Ended | Year Ended | ||||||||||||||||||||||||||

| December 31, 2011 |

December 31, 2012 |

March 31, 2013 |

June 30, 2013 |

September 30, 2013 |

December 31, 2013 |

December 31, 2013 |

||||||||||||||||||||||

| Revenue |

$ | 29,186 | $ | 125,121 | $ | 78,230 | $ | 95,360 | $ | 152,616 | $ | 215,183 | $ | 541,389 | ||||||||||||||

| Direct expense |

||||||||||||||||||||||||||||

| Transportation services |

24,434 | 108,507 | 67,957 | 82,705 | 124,804 | 169,253 | 444,719 | |||||||||||||||||||||

| Other direct expense |

55 | 489 | 207 | 88 | 162 | 118 | 575 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total direct expense |

24,489 | 108,996 | 68,164 | 82,793 | 124,966 | 169,371 | 445,294 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Gross margin |

4,697 | 16,125 | 10,066 | 12,567 | 27,650 | 45,812 | 96,095 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| SG&A expense |

||||||||||||||||||||||||||||

| Salaries & benefits |

2,484 | 15,171 | 10,163 | 12,367 | 17,559 | 24,784 | 64,873 | |||||||||||||||||||||

| Other SG&A expense |

716 | 3,590 | 1,895 | 3,031 | 6,626 | 8,637 | 20,189 | |||||||||||||||||||||

| Purchased services |

148 | 1,695 | 814 | 979 | 2,269 | 3,501 | 7,563 | |||||||||||||||||||||

| Depreciation and amortization |

44 | 1,223 | 1,014 | 1,180 | 4,611 | 8,087 | 14,892 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total SG&A expense |

3,392 | 21,679 | 13,886 | 17,557 | 31,065 | 45,009 | 107,517 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Operating income (loss) |

$ | 1,305 | $ | (5,554 | ) | $ | (3,820 | ) | $ | (4,990 | ) | $ | (3,415 | ) | $ | 803 | $ | (11,422 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| AS CONFORMED | For the | For the | For the | |||||||||||||||||||||||||

| Year Ended | Three Months Ended | Year Ended | ||||||||||||||||||||||||||

| December 31, 2011 |

December 31, 2012 |

March 31, 2013 |

June 30, 2013 |

September 30, 2013 |

December 31, 2013 |

December 31, 2013 |

||||||||||||||||||||||

| Revenue |

$ | 29,186 | $ | 125,121 | $ | 78,230 | $ | 95,360 | $ | 152,616 | $ | 215,183 | $ | 541,389 | ||||||||||||||

| Cost of purchased transportation and services |

24,489 | 108,996 | 68,164 | 82,793 | 124,966 | 169,371 | 445,294 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net revenue |

4,697 | 16,125 | 10,066 | 12,567 | 27,650 | 45,812 | 96,095 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Direct operating expense |

0 | 0 | 0 | 0 | 2,077 | 4,278 | 6,355 | |||||||||||||||||||||

| SG&A expense |

||||||||||||||||||||||||||||

| Salaries & benefits |

2,484 | 15,171 | 10,163 | 12,367 | 17,442 | 24,554 | 64,526 | |||||||||||||||||||||

| Other SG&A expense |

716 | 3,590 | 1,895 | 3,031 | 5,172 | 6,022 | 16,120 | |||||||||||||||||||||

| Purchased services |

148 | 1,695 | 814 | 979 | 1,763 | 2,068 | 5,624 | |||||||||||||||||||||

| Depreciation and amortization |

44 | 1,223 | 1,014 | 1,180 | 4,611 | 8,087 | 14,892 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total SG&A expense |

3,392 | 21,679 | 13,886 | 17,557 | 28,988 | 40,731 | 101,162 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Operating income (loss) |

$ | 1,305 | $ | (5,554 | ) | $ | (3,820 | ) | $ | (4,990 | ) | $ | (3,415 | ) | $ | 803 | $ | (11,422 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

Management Presentation

May 1, 2014

Exhibit 99.2 |

2

Forward-Looking Statements Disclaimer

This document includes forward-looking statements within the meaning of Section 27A of the

Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as

amended, including the company’s full year 2014 and full year 2017 financial targets and

expected cost synergies from the Pacer integration. All statements other than statements of historical

fact are, or may be deemed to be, forward- looking statements. In some cases,

forward-looking statements can be identified by the use of forward-looking terms such as "anticipate,"

"estimate," "believe," "continue," "could," "intend,"

"may," "plan," "potential," "predict," "should," "will," "expect," "objective," "projection," "forecast,"

"goal," "guidance," "outlook," "effort," "target" or the

negative of these terms or other comparable terms. However, the absence of these words does not

mean that the statements are not forward-looking. These forward-looking statements are based on certain assumptions and analyses

made by us in light of our experience and our perception of historical trends, current conditions and

expected future developments, as well as other factors we believe are appropriate in the

circumstances. These forward-looking statements are subject to known and unknown risks, uncertainties and

assumptions that may cause actual results, levels of activity, performance or achievements to

be materially different from any future results, levels of activity, performance or achievements

expressed or implied by such forward-looking statements. Factors that might cause or contribute to

a material difference include, but are not limited to, those discussed in XPO’s filings

with the SEC and the following: economic conditions generally; competition; XPO’s ability to find

suitable acquisition candidates and execute its acquisition strategy; the expected impact of

acquisitions, including the expected impact on XPO’s results of operations; XPO’s

ability to raise debt and equity capital; XPO’s ability to attract and retain key employees to execute its growth

strategy; litigation, including litigation related to alleged misclassification of independent

contractors; the ability to develop and implement a suitable information technology

system; the ability to maintain positive relationships with XPO’s networks of third-party transportation providers;

the ability to retain XPO’s and acquired businesses’ largest customers; XPO’s ability

to successfully integrate acquired businesses and realize anticipated synergies and cost

savings; rail and other network changes; weather and other service disruptions; and governmental regulation. All

forward-looking statements set forth in this document are qualified by these cautionary statements

and there can be no assurance that the actual results or developments anticipated will be

realized or, even if substantially realized, that they will have the expected consequences to, or effects

on, XPO or its businesses or operations. Forward-looking statements set forth in this document

speak only as of the date hereof, and XPO undertakes no obligation to update

forward-looking statements to reflect subsequent events or circumstances, changes in expectations or the

occurrence of unanticipated events except to the extent required by law.

|

3

One of the Largest 3PLs in North America

We facilitate over 25,000 deliveries per day

Sources for rankings: Transport Topics, Journal of Commerce and company data

#4 freight brokerage firm and Top 50 logistics company

#3 provider of intermodal services

#1 provider of cross-border Mexico intermodal

#1 manager of expedited shipments

#1 provider of last-mile logistics for heavy goods

International and domestic freight forwarder

Growing presence in managed transportation and LTL |

4

Clearly Defined Strategy for Value Creation

Acquire companies that bring value and are highly scalable

Significantly scale up and optimize existing operations

Open cold-starts where sales recruitment can drive revenue

We continue to be on track or ahead of plan

with all three legs of our growth strategy |

5

Completed 11 strategic acquisitions and established

24 cold-starts in two years

Created leading-edge recruiting and training programs

Introduced scalable IT platform

Added national operations centers for shared services, carrier

procurement and last-mile operations

Stratified customers, assigned a single point of contact to each

Created a culture of passionate on-time performance

Disciplined focus on operational excellence

Precise Execution of Growth Plan |

6

Massive Commitment to Shipper Satisfaction

Integrated network across North America with global reach

–

Primarily in the manufacturing, industrial, retail, food and

beverage, commercial, life sciences and government sectors

123 locations in the U.S., Canada, Mexico, Asia and Europe

Approximately 3,000 employees

Over 14,000 customers

More than 1,000 owner-operator trucks under contract for

drayage and expedited subsidiaries

Relationships with an additional 26,000 vetted carriers

|

7

Significant Growth Embedded in XPO’s Model

Strategic

accounts:

market

to

large

shippers

Cold-starts:

expand

footprint

in

markets

with

best

access

to sales talent

Scale

and

productivity:

recruit

sales

reps

and

provide

state-

of-the-art training and IT

Supply

chain

offering:

build

leadership

positions

in

the

fastest-growing areas of logistics

Performance:

become

the

logistics

partner

of

choice

due

to

our relentless focus on on-time pickup and delivery

M&A

program:

focus

on

the

top

100

pipeline

prospects |

8

Leading Positions in High-Growth Sectors

Sources: Armstrong & Associates, Norbridge, Inc., EVE Partners LLC, FTR

Associates, SJ Consulting Group, Inc., Bureau of Economic Analysis, US

Department of Commerce Sector

Market

Size

($ billions)

Projected

Growth

(x GDP)

Growth Drivers

Truck brokerage

$50

2-3 times

Outsourcing and technology

Intermodal

$15

3-5 times

Long-haul rail efficiencies and

near-sourcing of

manufacturing in Mexico

Heavy goods,

last-mile

$13

5-6 times

Outsourcing and e-commerce |

9

Comprehensive North American Network

Source: Company data

123 locations

Approximately 3,000

employees

Over 26,000 active,

vetted carriers

Access to 60,000 miles

of network rail routes |

10

Acquired Pacer in March 2014

Provides instant scale in the $15 billion intermodal sector,

the fastest-growing freight mode in North America

–

Third largest provider of intermodal services

–

Largest provider of cross-border Mexico intermodal

Enhances XPO’s value proposition as a large, single-source

supply chain partner with deep capacity

Creates company-wide cross-selling opportunities in every

area of XPO service

Access to 60,000 miles of network rail routes

Sources: SJ Consulting Group, Inc., American Trucking

Associations and company data |

11

Largest provider of heavy goods, last-mile logistics in

North America

High value, high margin business, growing rapidly due to

e-commerce and outsourcing

Strengthens XPO’s position with shippers as a large,

single-source provider

Industry-leading customer experience IT can be used by XPO

Acquired Optima Service Solutions in November 2013

–

Highly scalable supplier to 3PD, leader in last-mile delivery

of large appliances and electronics

Acquired 3PD in August 2013 |

12

XPO NLM is the largest manager of expedited shipments

in North America

Acquired NLM in December 2013

#1 provider of web-based transportation management

for expedited

Managing over $1 billion of annual gross transportation spend

–

Online auction system proprietary to XPO

–

Carriers bid on loads that are awarded electronically

Benefits from trend toward just-in-time inventories, and supply

chain disruptions |

13

Focused Sales and Marketing Effort

Differentiate XPO by providing a passionate commitment to

customer satisfaction across a range of services

Single point of contact for each customer

–

Strategic accounts team marketing to largest 2,000 shippers

–

National accounts team focused on next largest

5,000 companies

–

Branch network expands our reach to hundreds of

thousands of small and medium-sized shippers

Capture more of the $32 billion less-than-truckload opportunity

Sources: SJ Consulting Group, Inc., company data |

14

One common IT platform for freight brokerage in all cold-starts

and acquired companies

Proprietary freight optimizer tools for pricing and load-covering

put in place in 2012

Highly scalable load execution and tendering via automated

load-to-carrier matching

Total IT budget of more than $70 million for 2014

(1)

Increasing Productivity through Technology

(1) Includes IT budget for Pacer |

15

24 cold-starts

–

11 in freight brokerage, including Kansas City opened

in March; 12 in freight forwarding; one in expedited

Brokerage cold-starts on an annual revenue run rate of more

than $190 million

–

Nearly triple the run rate 12 months ago

Low capital investment can deliver outsized returns

Hire strong industry veterans as branch presidents

Position in prime recruitment areas and scale up

Growth through Cold-starts |

16

Founded and led four highly successful companies,

including world-class public corporations

Amerex

Oil

Associates:

Built

one

of

world’s

largest

oil

brokerage

firms

Hamilton

Resources:

Grew

global

oil

trading

company

to

~$1

billion

United

Waste:

Created

5th

largest

solid

waste

business

in

North

America

United

Rentals:

Built

world’s

largest

equipment

rental

company

United Waste stock outperformed S&P 500 by 5.6x from 1992 to 1997

United Rentals stock outperformed S&P 500 by 2.2x from 1997 to 2007

CEO Bradley S. Jacobs |

17

Highly Skilled Management Team

Partial list

The full management team can be found on www.xpologistics.com

Sean Fernandez

Chief Operating Officer

Tom Connolly

Senior Vice President, Acquisitions

Karl Meyer

Chief Executive Officer, 3PD division

Julie Luna

Chief Commercial Officer

John Hardig

Chief Financial Officer

Lou Amo

Vice President, Carrier Procurement

Dave Rowe

Chief Technology Officer

Mario Harik

Chief Information Officer

Gordon Devens

General Counsel

Scott Malat

Chief Strategy Officer

Troy Cooper

Senior Vice President, Operations and Finance

NCR, Avery Dennison, Arrow Electronics

EVE Partners

Pacer International, Union Pacific

Stifel Nicolaus, Alex. Brown

Electrolux, Union Pacific, Odyssey Logistics

Echo Global Logistics

Oakleaf Waste Management

United Rentals, United Waste

Goldman Sachs, UBS, JPMorgan Chase

AutoNation, Skadden Arps

3PD, Inc., Home Depot |

18

Deep Bench of Industry Experience Partial list

Jake Schnell

Sr. Operational Process and Integration Manager

Jenna Sargent

Regional Sales and Operation Manager

Marie Fields

Director of Training

Evan Laskaris

Director of Operations, Chicago

Chris Healy

President, Expedited Transportation

Jim Commiskey

Strategic Accounts Manager

Gregory Ritter

Senior Vice President, Strategic Accounts

Doug George

Branch President, Dallas

Will O’Shea

Chief Sales and Marketing Officer, 3PD division

Andrew Armstrong

Sales and Operations Manager

Drew Wilkerson

Branch President, Charlotte

Boyd Brothers, Caliber Logistics, Roberts Express

C.H. Robinson

OHL, Schneider Logistics

C.H. Robinson, American Backhaulers

AFN, CEVA Logistics, Menlo

Pacer International, UPS, Menlo

Knight Brokerage, C.H. Robinson

AFN, Ryder Integrated Logistics

Livingston International, Echo Global Logistics

C.H. Robinson

Ryder Integrated Logistics, Cardinal Logistics |

19

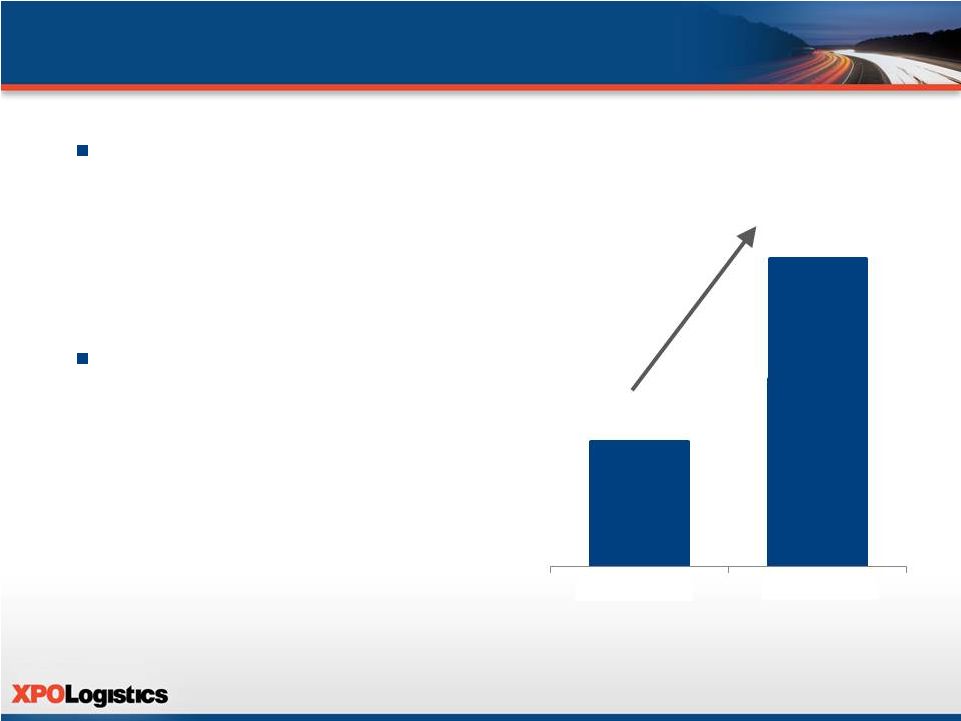

Revenue trajectory

–

2011 revenue of $177 million

–

Currently at approximately $2

billion annual revenue run rate

1Q growth company-wide, 2014

vs. 2013

–

Organic growth up 51%

–

Gross revenue up 148%

–

Net revenue up 259%

Revenue and Margin Growth

Source: Company data

Revenue ($ millions)

+148%

$114

$282

Q1 2013

Q1 2014 |

20

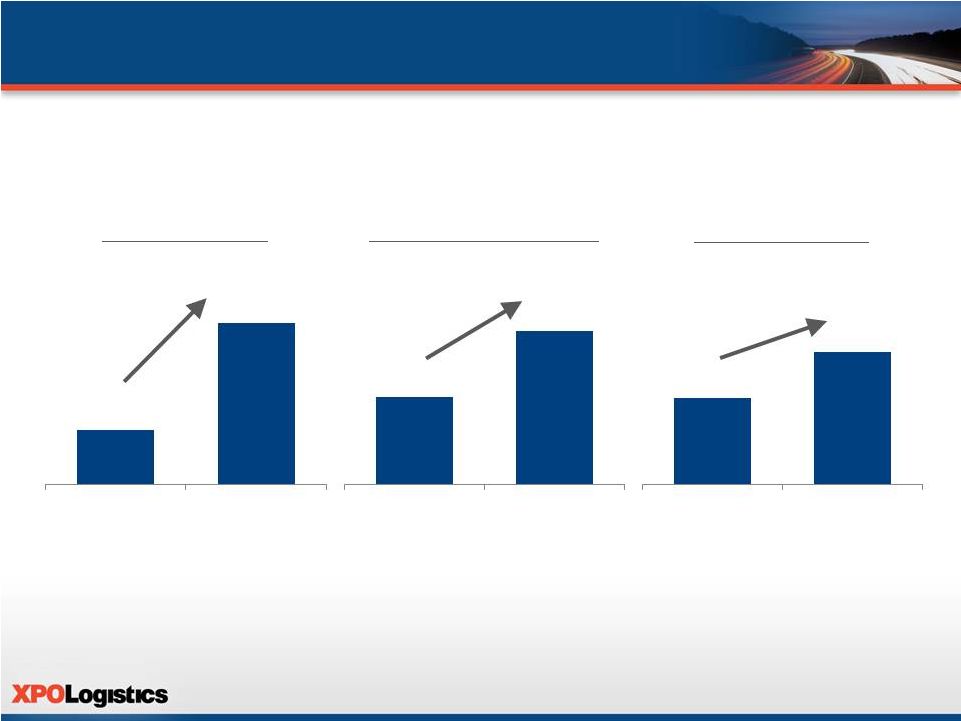

Key Financial Statistics

Expedited

Transportation

Freight Brokerage

Freight Forwarding

+196%

+42%

+20%

1Q revenue growth by business unit, 2014 vs. 2013

Organic growth

up 75%

34% margin,

up from 16%

48% increase in

operating income

Revenue ($ millions)

$78

$232

Q1 '13

Q1 '14

$24

$34

Q1 '13

Q1 '14

$16

$20

Q1 '13

Q1 '14 |

21

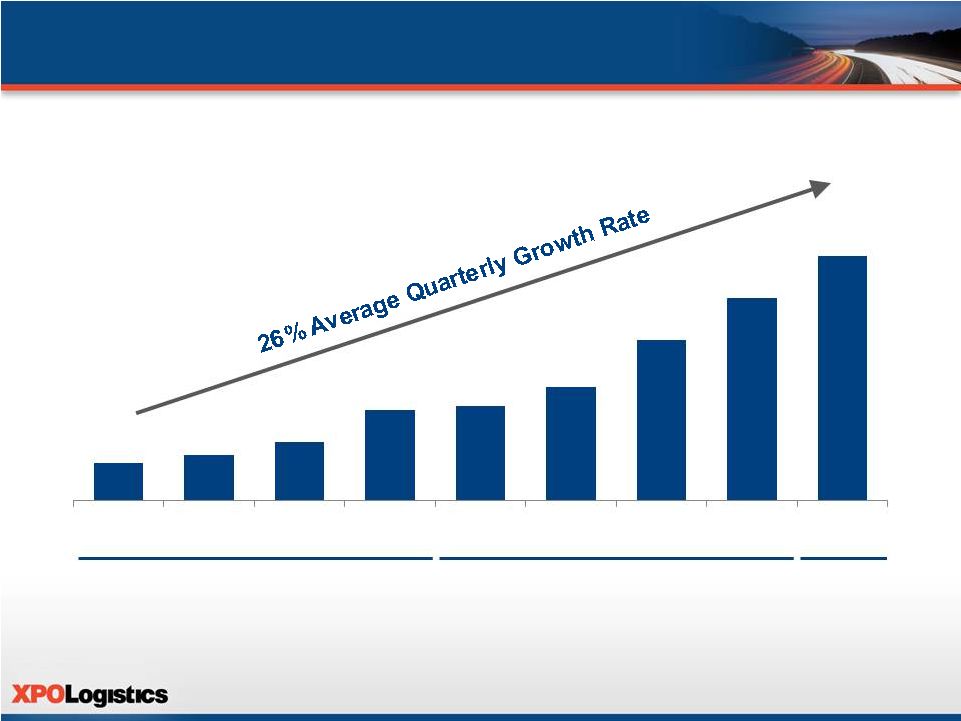

First 27 Months of Growth Strategy

Source: Company data

Revenue ($ millions)

2012

2013

2014

$45

$55

$71

$109

$114

$137

$194

$257

$282

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1 |

22

Full year 2014

Annual revenue run rate of at least $2.75 billion by

December

31

Annual EBITDA run rate of at least $100 million by

December

31

At least $400 million of acquired historical annual revenue,

excluding the Pacer acquisition

Full year 2017

Revenue of $7.5 billion

EBITDA of $425 million

Financial Targets |

23

Incentivized XPO Management

Equity ownership aligns management team with shareholders

Management

and

directors

own

approx.

29%

of

the

company

(1)

Common Stock Equivalent Capitalization as of 4/30/14

Common Shares

52.5 million

Preferred Shares

10.5 million

Warrants (Strike Price $7 per share)

10.6

million

(7.8

million

dilutive)

(2)

Convertible Senior Notes

7.3

million

shares

(3)

Stock Options and RSUs

2.3

million

shares

dilutive

(4)

Fully Diluted Shares Outstanding

80.4 million shares

Based on SEC beneficial ownership calculation as of April 30, 2014 Dilutive effect

of warrants calculated using treasury method (market close price of $27.14 as of 4/30/14); total warrant proceeds of $74.0 million

Assumes conversion in full of $120.7 million in aggregate principal amount of outstanding 4.50%

convertible senior notes due 2017

As of April 30, 2014, dilutive effect of outstanding RSUs and stock options calculated using treasury

method (market close price of $27.14 as of 4/30/14)

(1)

(2)

(3)

(4) |

24

Significant growth embedded in XPO’s business model

Leading positions in fastest-growing areas of transportation

Compelling multi-modal value proposition for shippers of

all sizes

Passionate culture of on-time performance and productivity

Top management talent with skills that uniquely fit

growth strategy

Positioned as an irreplaceable, single-source provider

Clear Path for Significant Value Creation |

Exhibit 99.3

May 1, 2014

Presentation Script

The following script should be read in conjunction with the accompanying slide presentation, which contains, among other information, source data for certain information set forth in the script.

Thank you very much for joining us. To start, for those of you who might not be familiar with XPO, here’s some information about our company and strategy. We’ll explain the drivers behind our 26% average quarterly growth rate over the last 27 months, and our 51% organic growth in the most recent quarter.

We took control of XPO Logistics in September of 2011, with the objective of building a world-class transportation logistics company under the new XPO Logistics brand. We put a highly skilled management team in place and began executing our disciplined strategy for growth:

| • | Acquire attractive companies that bring value and are highly scalable; |

| • | Optimize our existing operations with vigorous recruitment and training programs and state-of-the-art IT; and |

| • | Open cold-starts in locations where we can hire a large number of qualified salespeople to drive returns. |

Today, we’re one of the fastest-growing logistics companies in North America, with a freight brokerage division that we’ve taken from a single location to the fourth largest brokerage firm in two years. We’re the largest provider of last-mile logistics, the largest manager of expedited shipments, and the third largest provider of intermodal services, with growing positions in managed transportation, freight forwarding and less-than-truckload brokerage.

We completed eleven acquisitions to date, including the billion-dollar Pacer business in March. We grew our headcount from barely 200 employees in late 2011 to approximately 3,000 and counting. We developed cutting-edge recruiting, training and onboarding programs. And we introduced a scalable IT platform, with three major upgrades and enhancements every few weeks.

We have a nationwide cold-start program underway with 24 locations operating under experienced leadership: 11 in freight brokerage, 12 in freight forwarding and one in expedite. Our drayage and expedited subsidiaries have more than 1,000 owner-operator trucks under contract. And our capacity procurement hubs in Charlotte, Chicago and Atlanta manage relationships with an additional 26,000 carriers, representing capacity of more than half a million trucks on the road.

Most important, we’ve instilled a high-octane, performance-driven culture focused on delivering world-class service to customers. Our sales and operations people know how to deal with customers on a professional basis, and we work to differentiate XPO by providing a consistently superior customer experience.

Our March acquisition of Pacer International is our fourth in the last eight months. In the last half of 2013, we bought 3PD and Optima – the largest providers in their last-mile sectors. And in December we acquired NLM, the leading online manager of expedited shipments. The addition of NLM to our expedited group made us the largest manager of expedited shipments in North America, and gave us an important foothold in managed transportation. We’ve made XPO a major player in the fastest-growing areas of logistics: last-mile logistics, for example, is growing at five to six times GDP, and intermodal is growing at three to five times GDP.

We’re bullish about the Pacer acquisition for a lot of reasons, but four in particular. First, the intermodal sector is one of the fastest-growing areas of transportation logistics. Second, it made us the third largest provider of intermodal services in North America. Third, we’re now the number one provider of intermodal services in the cross-border Mexico marketplace, which is exhibiting strong growth trends. And fourth, the combination has created growth opportunities in every area of our service offering.

Intermodal is a dynamic, $15 billion sector that has been growing at three to five times GDP. Many shippers are discovering that they can use intermodal to lower their transportation costs for freight that travels at least 600 miles or so, in part because rail can be up to three times more fuel-efficient than truck for long haul. Currently, more than a third of our over-the-road freight movements travel over 600 miles – that could make them ripe for conversion to intermodal.

Cross-border Mexico is a high-growth sector of intermodal, driven by a shift to near-shoring by manufacturers. Mexico offers a competitively priced labor force and greater speed-to-market than overseas locales such as China – and compared to truckload, rail can offer a more cost-effective way to move freight cross-border. In addition, the Mexican government and railroads have made significant investments in the country’s transportation infrastructure. It’s estimated that approximately 2.8 million trucks move cross-border each year, so there’s a large potential universe for conversion to rail.

In addition to these revenue opportunities, the Pacer acquisition offers significant cost synergies. Our updated estimate for synergies from the integration has tripled from our initial expectations. We now expect to realize $15 million of synergies in technology, real estate, sales and administrative functions, public company costs, and duplicative personnel – and we’ve already executed on many of them.

For example, we quickly implemented our plan to reverse the losses of Pacer’s logistics business. We closed or consolidated 16 offices and retained 10 profitable operations as part of our XPO Global Logistics freight forwarding group. Dominick Muzi, who’s done a superb job at ramping up our profitability in freight forwarding over the last three years, is now in charge of growing this combined organization.

We put the former Pacer truck brokerage business under the leadership of Josh Allen, and fully integrated it with XPO. Josh is one of our regional VPs – he’s been growing our brokerage offices in Louisville and Cincinnati at a fast clip. We moved the operations onto our proprietary Freight Optimizer technology, which has allowed the team to serve customers better and price loads more effectively. They can do their job faster on our more user-friendly system, with access to our more than 26,000 carrier relationships.

Our purchase of Pacer increased XPO’s sales and service network to approximately 3,000 employees at 123 locations. We’re facilitating more than 25,000 deliveries a day for our

2

customers, many of whom are enthusiastic about taking advantage of our expanded range of services. We’re in a strong position to leverage an important industry trend: many customers, particularly large shippers, want to winnow down their relationships to fewer, larger 3PLs with deep capacity across a range of services. We’re being responsive to the services our customers need and want by becoming a source of deep capacity across all major modes of transportation.

Those are the highlights of the Pacer acquisition and the potential upside it represents. Now let’s take a closer look at each part of our strategy and the significant growth that’s embedded in our business model.

First is scale and optimization. This starts with our industry fundamentals. The transportation logistics industry in the United States alone is about a trillion dollars annually. Over-the-road trucking is about $350 billion of that spend, with an estimated 15% penetration rate by brokers. This equates to a $50 billion opportunity that’s growing at about two to three times GDP. Currently, we have more than 14,000 customers, primarily in manufacturing, industrial, retail, commercial, life sciences and government-related accounts – yet we serve less than 2% of the addressable market.

One thing that’s likely to drive increased penetration is an outsourcing trend with both shippers and carriers. It makes economic sense for carriers to find loads through brokers instead of carrying the costs of an internal sales team. And shippers – including those with direct carrier relationships – need large 3PLs as a source of critical capacity when trucks are hard to find. We’ve positioned our company to benefit from this long-term trend. We’re building XPO not just for the $50 billion that’s going through brokers right now, but for the $300 billion that’s currently going direct from shippers to carriers.

In addition to being large and growing, our industry is highly fragmented. There are more than 10,000 licensed brokers in the U.S., but only about 25 brokerage firms with more than $200 million in revenue. Fragmentation gives us a dual benefit: it supports the acquisition leg of our strategy, and creates a competitive advantage for XPO as one of the largest brokerage firms in North America.

We’re working diligently to raise our profile in front of every prospective customer in this space. We’ve identified the 2,000 largest shippers in North America as strategic account targets. The next largest 5,000 shippers are our national account targets. In addition, there are hundreds of thousands of small and medium-sized customers who can use our services. Our branch network reaches out to them every day.

We see huge growth potential in strategic accounts. Last year, we launched a strategic accounts team to target opportunities with the largest shippers. Every one of our strategic account managers has deep industry experience, and a long track record with large shippers. They’re very attentive to the nuances of the needs of large shippers, and they’re getting a favorable response from these customers – in the first quarter alone, we’ve signed business with 33 new strategic accounts.