UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934

Date of Report

(Date of earliest event reported):

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation) |

(Commission File Number) | (I.R.S. Employer Identification No.) |

(Address of principal executive offices)

(

(Registrant’s telephone number, including area code)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) | ||

| Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) | ||

| Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) | ||

| Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||

| Indicate by check mark whether the registrant is an emerging growth company as defined in as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter). |

| Emerging growth company |

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨ |

Item 7.01. Regulation FD Disclosure.

On May 3, 2021, XPO Logistics, Inc. (the “Company”) released a slide presentation expected to be used by the Company in connection with certain future investor presentations, together with a corresponding script. Copies of the script and slide presentation are attached as Exhibit 99.1 and Exhibit 99.2, respectively, to this Current Report on Form 8-K.

The slide presentation and script should be read together and with the Company’s filings with the Securities and Exchange Commission, including the Quarterly Report on Form 10-Q for the fiscal quarter ended March 31, 2021.

The information furnished in this Item 7.01, including Exhibit 99.1 and Exhibit 99.2, shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that Section, and shall not be deemed to be incorporated by reference into any filing of the Company under the Exchange Act or the Securities Act of 1933, as amended, except to the extent that the registrant specifically incorporates any such information by reference.

| Item 9.01. | Financial Statements and Exhibits. | |

(d) Exhibits

| Exhibit No. | Exhibit Description | |||

| 99.1 | Investor Presentation Script, dated May 3, 2021 | |||

| 99.2 | Investor Presentation, dated May 3, 2021 | |||

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document) | |||

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Date: May 3, 2021 | XPO LOGISTICS, INC. | |

| By: | /s/ Karlis P. Kirsis | |

| Karlis P. Kirsis | ||

| Corporate Secretary | ||

|

Exhibit 99.1 |

May 3, 2021

Presentation Script and Slides

The following script should be read in conjunction with the accompanying slide presentation, which contains, among other information, source data for certain information set forth in the script.

Thank you for joining us. We’ll start with an overview of XPO Logistics today, and our strategy for driving growth, competitive differentiation and financial returns. We’ll also bring you up to date on some recent developments, including the planned spin-off of our logistics business. And we’ll give you an overview of our record first quarter financial performance, which further increased our momentum after a dramatic rebound from the impact of COVID-19 in 2020.

XPO is one of the largest providers of supply chain services in the world, with over $16 billion in 2020 revenue and an integrated network of people, technology and physical assets. We have 1,621 locations in 30 countries and approximately 140,000 team members, comprised of 108,000 employees and 32,000 temporary workers. We use our network to help over 50,000 customers operate their supply chains most efficiently.

Our company has two reporting segments: transportation and logistics, each with leadership positions and robust growth prospects. In our transportation segment, we’re a top three less-than-truckload (LTL) provider in North America and the second largest freight brokerage provider globally. In our logistics segment, we’re the second largest contract logistics provider worldwide. Within each segment, our markets are highly diversified and we’re positioned to capitalize on fast-growing areas of demand. Approximately 62% of our 2020 revenue came from our transportation segment, and the remaining 38% came from our logistics segment.

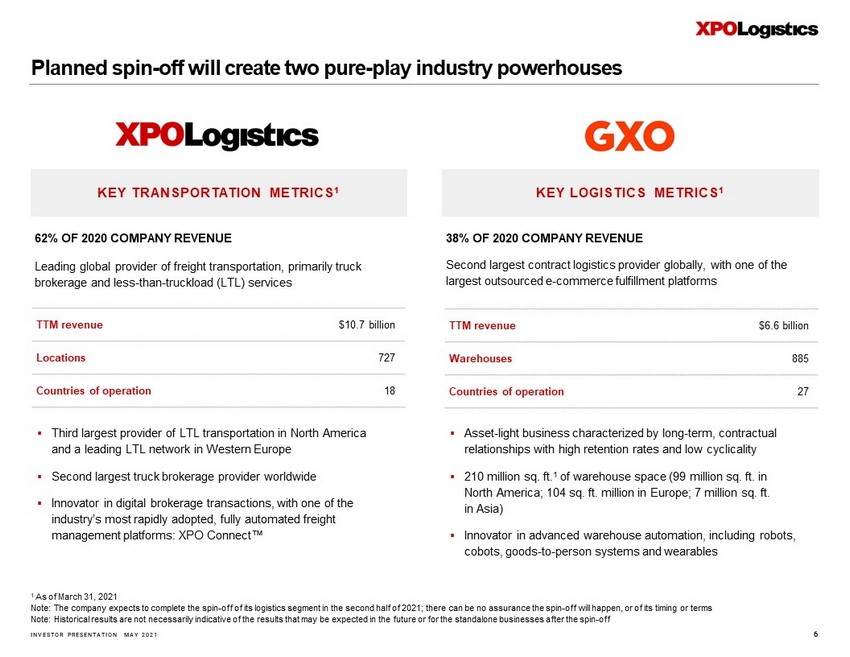

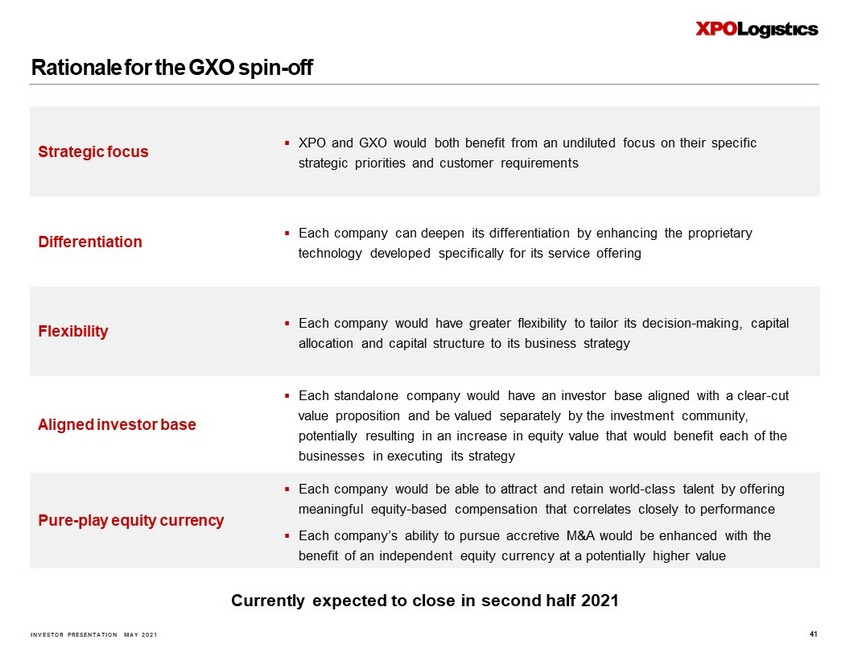

In December, we announced that we plan to spin off our logistics segment later this year as a separate publicly traded company. The spin-off — named GXO Logistics — will create two, pure-play industry leaders: GXO will be the second largest contract logistics provider in the world, and the remaining company will be a global provider of less-than-truckload and truck brokerage transportation services. We expect to complete the transaction in the second half of 2021.

We’re confident that the spin-off, if completed as planned, will enhance the growth prospects of both businesses. Each company will have greater flexibility to tailor strategic decision-making and capital allocations to their end-markets, with the benefit of strong positioning as customer-focused innovators. Each will have its own investor base and pure-play equity currency it can use to attract and retain world-class talent and pursue M&A. We’re in discussions with the rating agencies about our plan to achieve an investment-grade rating for GXO from day one, with XPO to follow.

1

The spin-off transaction is subject to various conditions, and may or may not occur, or its terms or timing may be different than originally planned.

Investor Highlights

These are the key factors driving our growth and returns companywide:

| · | We’re a global leader in logistics and truck brokerage, and a North American leader in less-than-truckload (LTL) transportation, with outsized exposure in verticals that have a history of enduring demand. |

| · | Our value proposition is a combination of scale, density, expertise and technology that gives us expansive opportunities for organic growth and share gains through accretive M&A. |

| · | In logistics, we’re strongly positioned to benefit from the industry’s predominant tailwinds — e-commerce and omnichannel retail, the shift toward supply chain outsourcing and warehouse automation. |

| · | In transportation, we have a best-in-class digital brokerage platform that’s driving profitable growth, while in LTL, our technology is expanding our margin, while the start of the rebound in the industrial economy is stimulating demand for our services. |

| · | Our rapid pace of innovation differentiates our service offerings and makes the most of the talent and assets within our organization. |

| · | Our scale gives us significant operating leverage, purchasing power, the capacity to innovate and the ability to deliver consistent outcomes across multiple markets for large customers. |

| · | We’re nimble allocators of capital, with a disciplined focus on returns and an enviable record of creating substantial shareholder value. |

| · | We serve customers in diverse verticals with complementary demand patterns, and the majority of our revenue is generated under long-term contracts, making our performance more resilient in economic cycles. |

| · | Our business model is optimized for free cash flow generation in all parts of the cycle; about 70% of our revenue is asset-light, with low maintenance capex. |

| · | Our secret sauce has always been the world-class people we attract to XPO — not just our 35 most senior executives, but also the 2,500 professionals at the next level with blue-chip industry experience. |

Technology Overview

One of the ways we strengthen our relationships with customers is by empowering our employees to deliver superior service through our technology. Our industry is evolving, and customers want to de-risk their supply chains with more automation and better visibility into the movement of their goods. We’re already well-positioned to meet this demand, because we prioritized digitization and visibility early in our technological development.

We’ve built a highly scalable platform on the cloud that speeds the deployment of new ways to increase efficiency, control costs and leverage our footprint. We can deploy innovations across multiple geographies in a relatively short time, and also take an innovation developed for one vertical and apply it to other verticals to differentiate the value we offer.

2

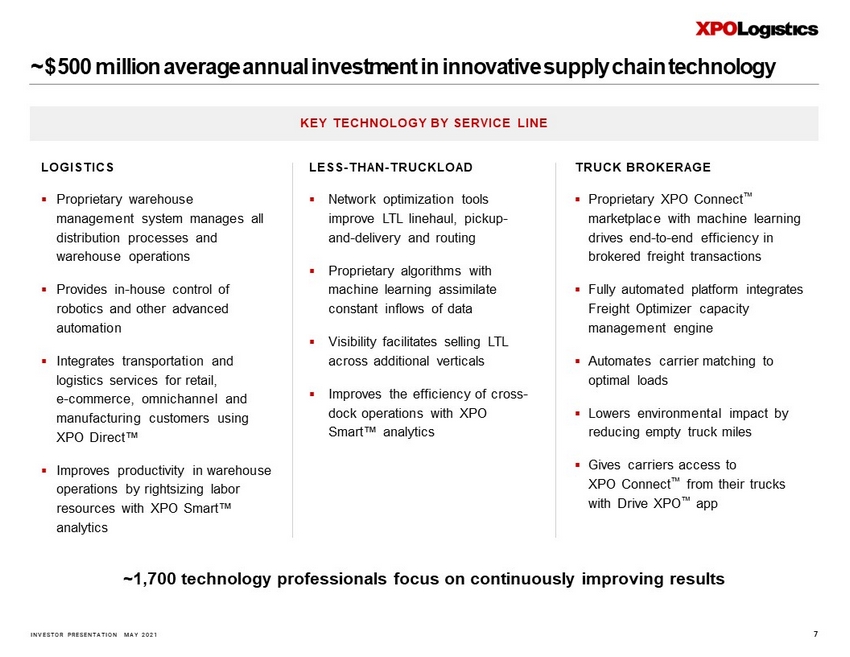

We believe that our investment in technology is among the highest in our industry at an annual average of about $500 million. We’re happy to make that commitment, because technology is a high-ROI investment for us, and one that drives our competitive advantage in both transportation and logistics. When our logistics segment spins off as GXO, it will continue to use the intellectual property we’ve developed for those operations through IP assignments and licensing agreements.

The supply chain industry is wide open for disruptive thinking and we’re driving positive change. The most significant impacts of our technology to date are in these four areas:

XPO Smart™

XPO Smart™ is our proprietary suite of workforce planning tools that improve productivity in our logistics sites and LTL docks. The tools help our site managers determine the best staffing levels by shift, day and week, with the optimal mix of full- and part-time labor. Our proprietary analytics “learn” the operations of a specific site and can forecast how a labor management decision today could affect productivity in a future period.

We’re seeing an average 5% to 7% productivity improvement from XPO Smart™ as we optimize our labor management in a safe and disciplined manner. To date, the tools have been implemented in 100% of our LTL dock operations, over 85% of our North American logistics sites and about 60% of our European logistics sites, with further roll-outs underway. We expect to realize a significant upside from these implementations as we fully utilize XPO Smart™ in our operations.

Intelligent warehouse automation

Intelligent warehouse automation is a priority for our logistics segment. This includes autonomous robots and collaborative robots (cobots), automated sortation systems, automated guided vehicles, goods-to-person systems and wearable smart devices. We integrate these technologies into our operations and control them in-house with our proprietary warehouse management system.

Advanced automation, robotics and autonomous goods-to-person systems are particularly effective in delivering critical improvements in speed, accuracy and productivity. Importantly, automation also enhances safety and the overall quality of employment.

In mid-2020, we opened a fully automated Digital Distribution Warehouse of the Future in the UK, which we co-developed with Nestlé, the world’s largest food and beverage company. This site has the capacity to process more than a million pallets per year — the highest throughput of any facility in Nestlé’s global network. Our European innovation lab is based on the premises, where it functions as both a think tank and a test site for new technologies.

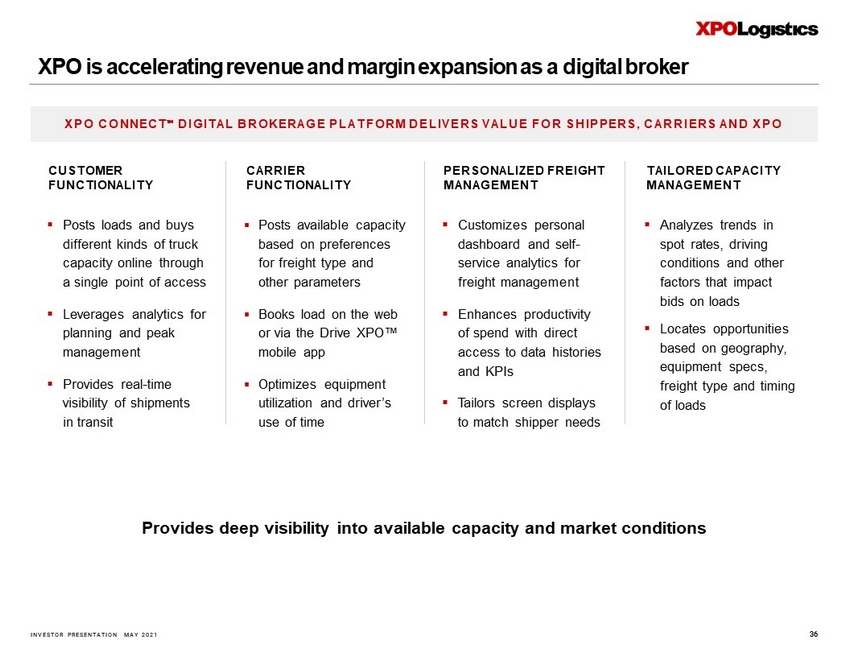

XPO Connect™

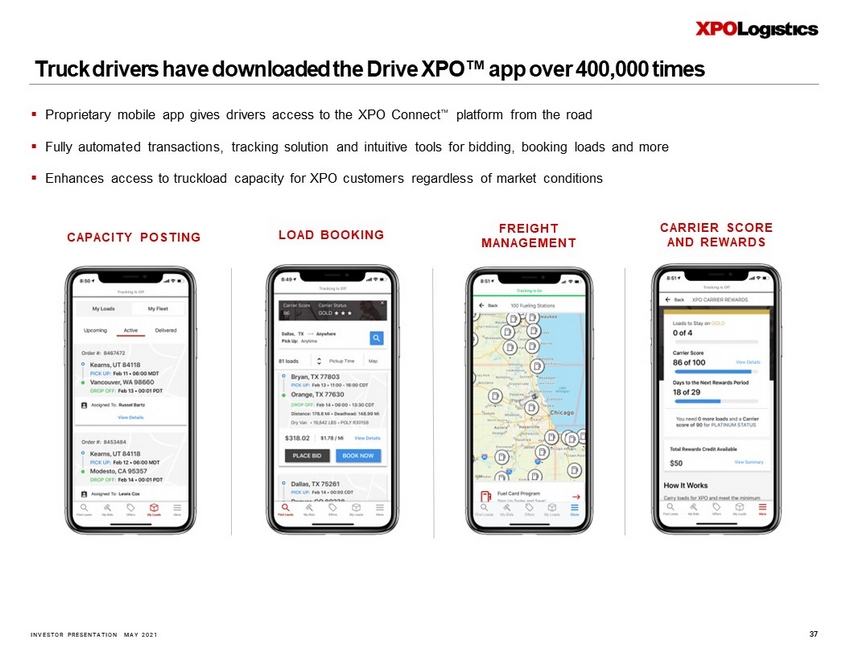

XPO Connect™ is our proprietary digital platform that fully automates transportation procurement — it encompasses our Freight Optimizer system, shipper interface, pricing engine, carrier interface and our carrier mobile app. When our customers have truckload freight to move, we use this powerful technology to find the optimal carrier based on a number of parameters, including price, market conditions and load profile.

3

Our investment in digitization is making our brokerage business much more efficient and reducing our costs. It enables us to capture share and elevate customer service without large increases in headcount. The technology gives our customers to the flexibility to source reliable truckload capacity at the optimal price, gain insights into market conditions and tender loads at their convenience. Carriers can increase their income and reduce empty miles by having their drivers bid on loads from their trucks, using our mobile app.

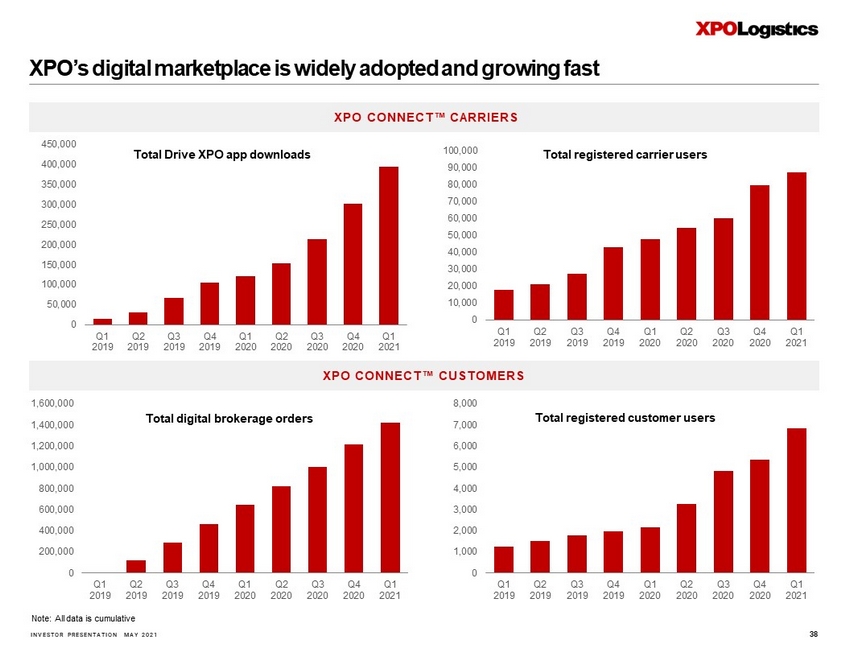

In the first quarter, we topped 81,000 truck carriers registered on XPO Connect™, which is an increase of 50% year-over-year. In April, we surpassed 400,000 truck driver downloads of the platform’s mobile app, up from 300,000 just three months earlier.

LTL optimization

In less-than-truckload, we’re growing our margin by innovating the way we operate. LTL is a rock-solid industry with strong fundamentals, which gives us the ability to focus our technology on optimizing specific components of the service we provide — primarily linehaul, pickup-and-delivery, pricing and dock productivity. For instance, with intelligent route-building, we can reduce empty miles in our linehaul network and mitigate cargo damage. To boost trailer utilization, our proprietary algorithms arrive at recommendations to fill trailer gaps based on volume and density, taking freight dimensions into account.

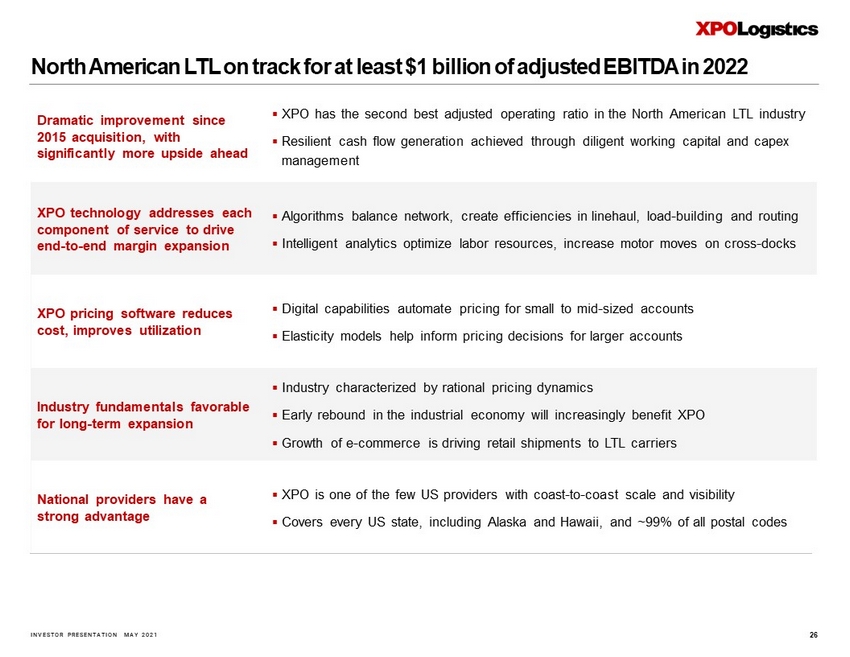

Our North American LTL linehaul network moved freight approximately 2.3 million miles a day on average in 2020, which is an enormous lever for efficiency and profitability. From 2015 to 2020, we improved the operating margin by 960 basis points, and we believe there’s a lot more we can gain.

Company Overview

We created XPO in 2011 to provide exceptional value for our customers while generating meaningful returns for our shareholders. The supply chain industry is vast, growing, fragmented and ripe for innovation, with underpenetrated sectors.

Supply chains are unique by nature. Each one is a network spanning every step a company must take to move its goods from the origin to the end-user. Our customers typically have supply chains that include vendors, manufacturers, labor, assets, technologies, data and other resources.

Our service offering is asset-light overall, with assets accounting for less than a third of revenue. In 2020, our net capex was 2% of revenue — a notably lower percentage than asset-intensive competitor groups in our industry, such as less-than-truckload, truckload, parcel and rail carriers. The assets we do own or lease are critical components of the customer services we provide, such as 885 logistics sites, and on the transportation side, 552 cross-docks and approximately 13,000 tractors and 35,000 trailers.

We market our service offerings using a two-pronged sales strategy: earn a greater share of wallet with our existing customer base and further penetrate high-growth verticals where our expertise and track record give us an advantage.

4

Over the past three years, we deepened our bench strength of senior-level sales talent in transportation and logistics in both North America and Europe. We also invested in new training and analytics for our salesforce and sales support personnel in North American LTL.

Overview of Logistics Operations

XPO is at the forefront of a $130 billion logistics industry in North America and Europe combined, of which we have about a 5% share. Our customers include many of the largest and most respected brands in the world — market leaders, such as Apple, Boeing, Coca Cola, Intel, L'Oréal, Nestlé and Nike. The average tenure of our top 20 logistics customers is 15 years.

Our logistics services are differentiated by our ability to deliver technology-enabled, customized solutions, vertical expertise, sophisticated engineering and scale — all of which make us attractive to national and multinational customers. Our footprint stands at approximately 210 million square feet (20 million square meters) of warehouse space.

Within our logistics segment, which we sometimes refer to as supply chain or contract logistics, we’ve identified these key drivers of value creation:

| · | Our strong positioning with blue-chip customers who require bespoke solutions, and our ability to grow with them, making a compelling case for outsourcing to us; |

| · | Leading capabilities for e-commerce and reverse logistics management, including the largest outsourced e-fulfillment platform in Europe and expansive capabilities for e-fulfillment, omnichannel logistics and returns management in North America; |

| · | Our robust technological differentiation, including our proprietary warehouse management platform that integrates robotics and other advanced automation to facilitate agility, visibility, speed, accuracy and control; |

| · | Our XPO Direct™ network — an innovative, shared-space distribution solution that gives customers a fluid way to position inventory close to target populations, reducing fixed costs and transit times; |

| · | A large opportunity to grow share in established specializations where we have a longstanding presence and relationships with sectors leaders; and |

| · | Significant levers for profitable growth and substantial free cash flow, with a long runway for margin expansion. |

Our logistics customers primarily operate in industries that are well-suited for outsourcing, including e-commerce and retail, food and beverage, consumer packaged goods, technology, aerospace, telecommunications, industrial and manufacturing, chemicals, agribusiness, life sciences and healthcare. These are all verticals where we have deep expertise and understand the specific requirements, such as special handling, complex stock-keeping, time-assured deliveries and surge management.

The e-commerce sector, in particular, continues to demonstrate strong, secular growth. Before COVID-19, e-commerce was already growing globally at a double-digit rate, and that growth has accelerated as more consumers opt to purchase goods online. Many retailers, e-tailers and direct-to-consumer manufacturers find it difficult to handle high volumes in-house without compromising service. The solutions we provide allow our customers to focus on their competencies and grow with confidence.

5

Many of our e-commerce facilities also manage merchandise returns, known as reverse logistics. This is one of the most highly valued services across multiple customer verticals. Reverse logistics services have become mission-critical for companies with consumer end-markets, as shoppers increasingly test-drive the products they buy online. Depending on the merchandise being returned, our services can include inspection, testing, repackaging, refurbishment, resale or product disposal, as well as refunding and warranty management.

Logistics processes overall are ripe for transformation through technology. Order fulfillment times are compressing, most notably in the direct-to-consumer space. The most cost-effective way to meet the majority of customer expectations is through advanced automation and intelligent machines — robots and cobots, automated sortation systems, automated guided vehicles and goods-to-person systems, which bring inventory to workers for order fulfillment.

We’ve been integrating collaborative robotics and goods-to-person systems into a number of our warehouses to support our employees and improve efficiency. We’re accelerating our deployment of automation, and this is substantially increasing throughput. In 2020, we shipped five times more product units using advanced warehouse robots than we did in 2019.

Robotics are particularly valuable in tight labor markets where wage inflation and labor shortages can erode customer margins. We’ve found that autonomous goods-to-person systems can improve productivity by 4-6x. Cobots, which assist workers with the inventory picking process, have a 2x benefit to productivity on average. Stationary robot arms can repeat demanding tasks with precision 3x faster than would be possible manually.

About 15% to 35% of consumer goods bought online are returned, depending on the product category. This creates peaks in returns at certain times of year. We’ve been able to shave several days off the reverse process through automation, which accelerates a customer’s ability to return goods to retail for sale.

In addition to our investments in automation and analytics, we’ve differentiated XPO from other logistics providers through our ability to create a synchronized warehouse environment across automation solutions. Our proprietary warehouse management platform integrates robotics and other advanced automation into our operations with rigorous control, even when complex, third-party software is involved.

Our XPO Smart™ workforce management tools are integrated into our warehouse ecosystem and deployed on the cloud. As logistics volumes fluctuate, our site leaders are able to make rapid adjustments to labor levels and improve productivity in real time.

XPO Direct™

XPO Direct™ is our shared-space distribution network for B2C and B2B customers in North America. This unique solution gives retailers, e-tailers and manufacturers a way to manage fulfillment using our scale, capacity and innovation without the need to add high-fixed-cost distribution centers. Our technology links our facilities, which serve as strategically located stockholding sites and cross-docks that can be utilized by multiple customers at the same time.

XPO Direct™ gives customers the flexibility to reposition inventory within one-day and two-day ground delivery range of approximately 99% of the U.S. population as demand patterns change, and in close proximity to retail stores for inventory replenishment. It gives our customers a strategic way to respond to consumer expectations for shorter fulfillment times and greater service agility. In addition, our customers have the use of our technology for distribution management and our analytics for demand forecasting.

6

Overview of Transportation Operations

Our other segment — transportation — derives the vast majority of its revenue and profit from less-than-truckload transportation, our largest transportation service line, and truck brokerage.

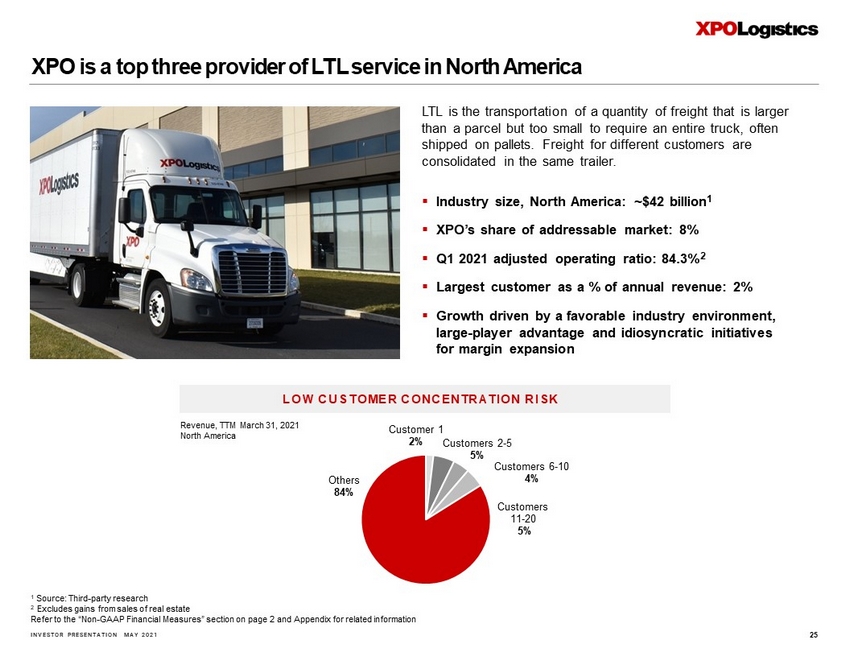

Less-Than-Truckload (LTL)

The company-specific drivers of growth and margin in our LTL business are:

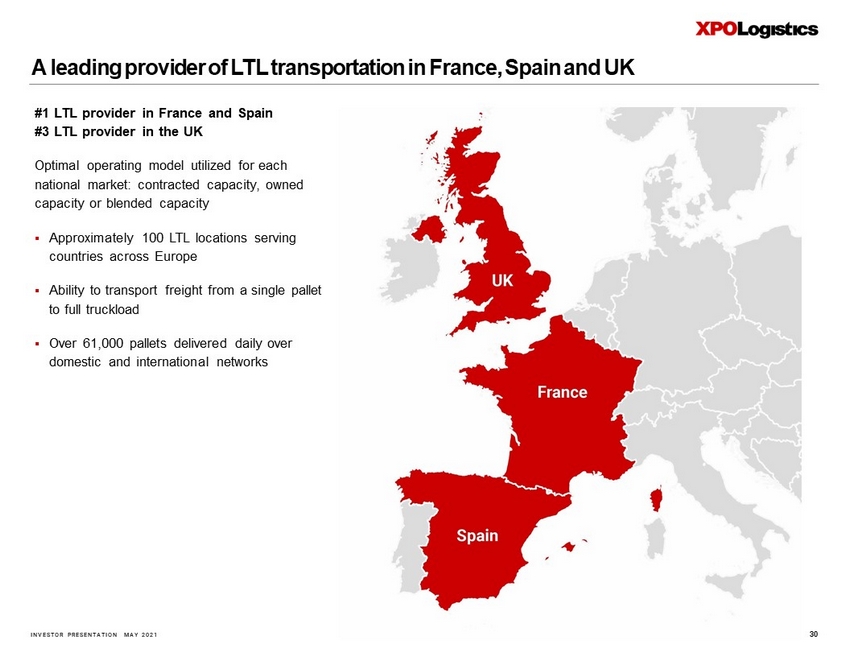

| · | Critical capacity and national lane density as the #3 LTL provider in North America, the #1 provider in France and Spain, and the #3 provider in the UK; |

| · | Sizable opportunities to further improve profitability beyond the significant gains we’ve already made by using our intelligent technology to optimize linehaul, pickup-and-delivery, pricing and variable labor spend; |

| · | Favorable industry fundamentals, including rational pricing dynamics in North America and the start of a recovery in industrial demand; and |

| · | Over 30 years’ experience and deep relationships with customers and partners in our domestic, cross-border and international networks. |

Our LTL operations in North America are asset-based. We provide customers with geographic density and day-definite regional, inter-regional and transcontinental LTL freight services with one of the industry’s largest fleets of tractors and trailers, professional drivers and a national network of terminals. This includes cross-border US service to and from Mexico and Canada, as well as intra-Canada service.

We doubled EBITDA in North American LTL within four years of acquiring this business in 2015, and we’ve brought the operation a long way forward. In the first quarter of 2021, our operating ratio was 84.9% and our adjusted operating ratio was 82.6%. Excluding gains from sales of real estate, our LTL adjusted operating ratio improved 220 basis points year-over-year to 84.3%. We’re on track to deliver at least $1 billion of LTL adjusted EBITDA in 2022.

Our LTL team is laser-focused on on-time, damage-free performance. Using one of the industry’s most modern fleets, we delivered approximately 12.4 million shipments in 2020. We have over 20,000 LTL customers in North America alone, primarily local accounts, and we’re diversifying our base by selling this service across more verticals.

Our linehaul network is how we move LTL freight across the country. We use intelligent route-building to increase linehaul fleet utilization, optimize load factor and limit cargo damage. To improve pickup-and-delivery performance, we developed routing and visualization tools that help our dispatchers leverage route density and reduce cost per stop. To optimize pricing, we use elasticity models to adjust for current lane conditions. And we use XPO Smart™ in our yard and dock operations to enhance productivity.

While each application of our technology delivers its own benefits, we also expect a strong synergistic effect on our LTL business as a whole. For example, when we optimize truck routes, this benefits asset utilization, driver utilization, customer service and yield, and should reduce our carbon footprint.

7

In Europe, where we’re a leading provider of LTL service in key markets, we utilize a blend of operations that includes asset-based (XPO fleet) and asset-light (contracted carriers), supported by a network of terminals. We have approximately 100 LTL locations serving countries across Europe, and we deliver over 61,000 pallets daily.

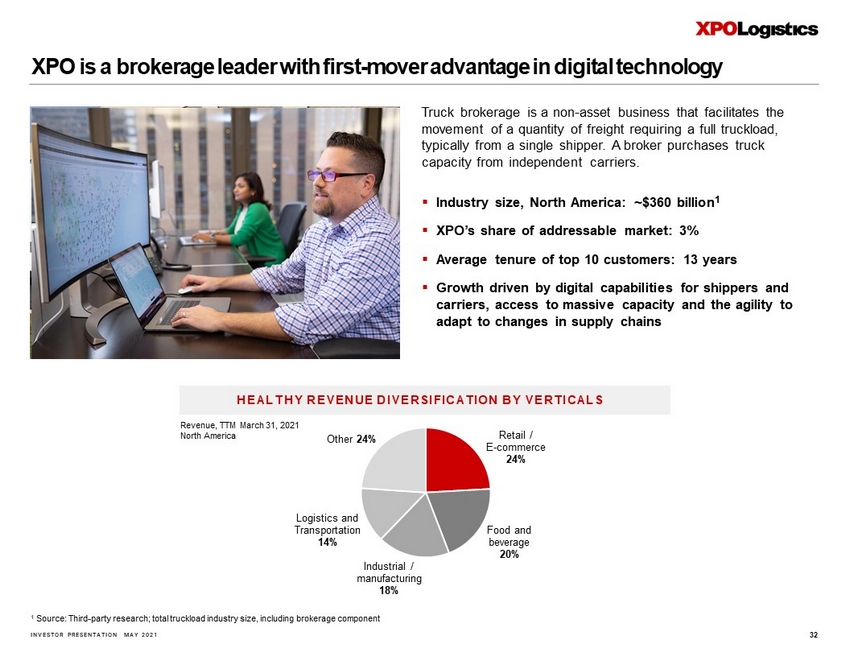

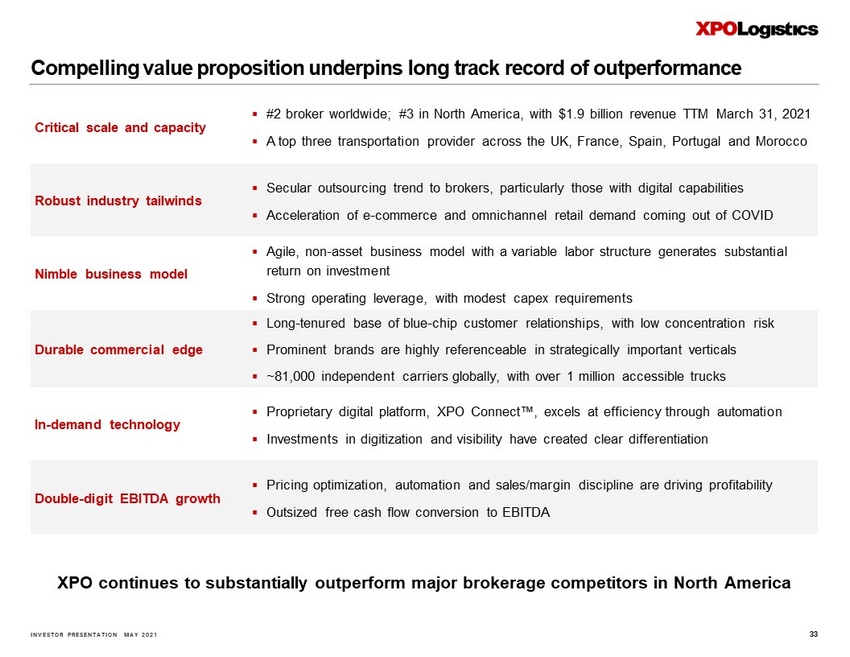

Truck Brokerage

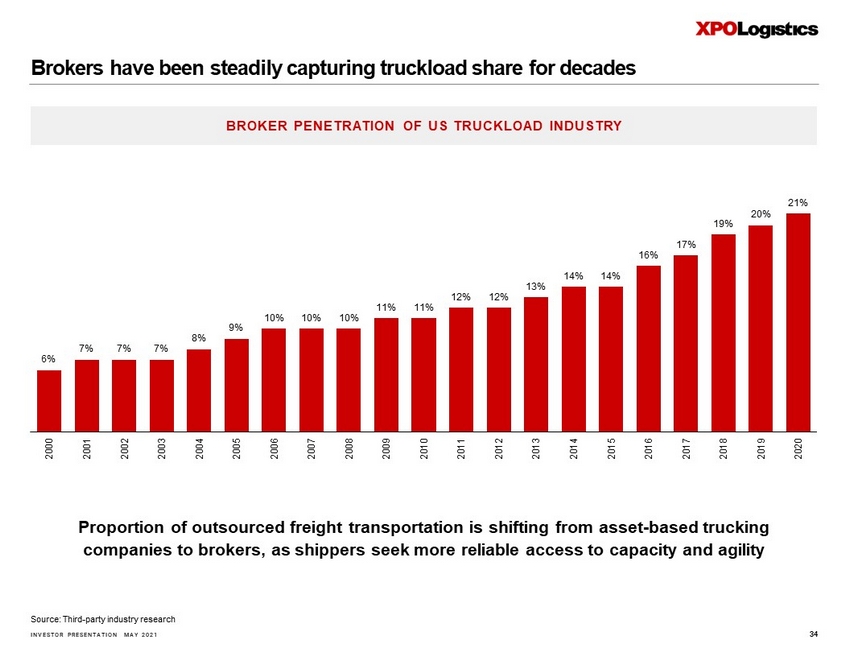

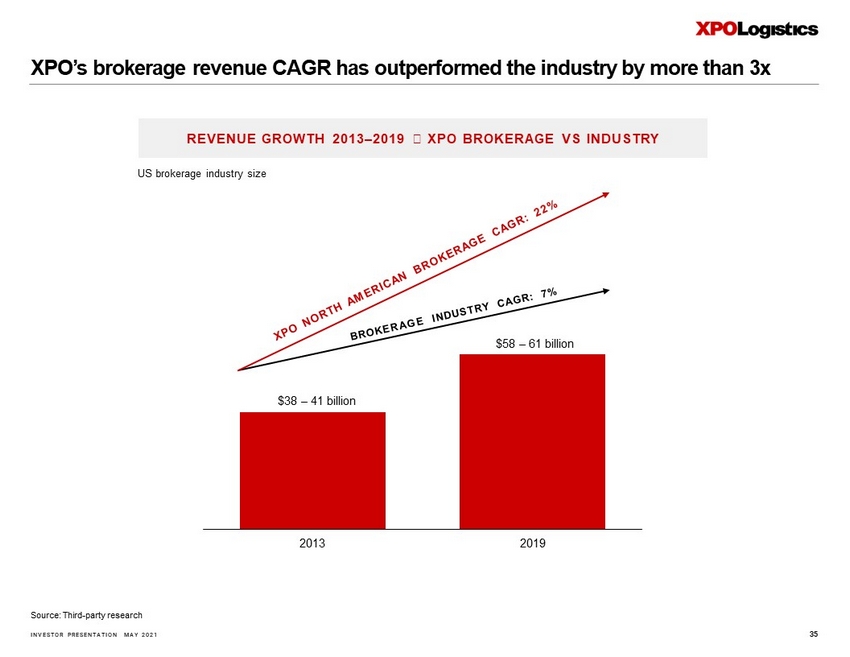

Our truck brokerage business has a long track record of outperformance — from 2013 through 2019, in the US, our revenue CAGR of 22% was more than three times the brokerage industry revenue CAGR of 7%. Our growth is being propelled by our scale and technology, and by favorable industry tailwinds:

| · | We offer customers critical capacity on a large scale as the #2 brokerage provider globally, the #3 broker in North America, and a top three transportation company across the UK, France, Spain, Portugal and Morocco; |

| · | Key secular trends are creating growth opportunities for us, including the growing demand for truckload capacity in the e-commerce and omnichannel retail sectors. Another trend is that shippers are increasingly outsourcing to brokers — particularly brokers with digital capabilities like XPO; |

| · | We have the opportunity to unlock incremental revenue and profit well beyond current levels through our XPO Connect™ digital marketplace, and capture high-margin opportunities with our pricing technology; and |

| · | Our long-tenured relationships with blue-chip customers are an opportunity to grow wallet share and leverage our reputation in key verticals. |

Our truck brokerage business has a nimble, non-asset model with a variable labor structure that generates substantial return on investment. We can reduce our costs when demand is soft and flex our resources to find trucks as demand returns. Essentially, we place shippers’ freight with qualified carriers, primarily trucking companies. This service is priced for shippers on either a spot market or contract basis. Customers offer loads to us daily via electronic data interchange, APIs, email, telephone and our XPO Connect™ platform.

As of March 31, 2021, we had approximately 81,000 independent carriers in our global brokerage network, giving us access to more than a million trucks. This enormous truckload capacity is a huge differentiator for us, together with our veteran brokerage leaders and our best-in-class technology.

XPO Connect™ has become one of the most rapidly adopted technologies in the brokerage industry. The value of the platform grows exponentially with every customer, carrier and transaction it touches. Importantly, it continually improves our brokerage service through automation, giving us the ability to manage volume growth without eroding margin.

Our transportation segment also includes an asset-light last mile logistics service for the home delivery of heavy goods — another sector that’s benefitting from the rapid expansion of e-commerce and omnichannel retail. XPO is the largest provider of last mile logistics for heavy goods in North America, with a growing last mile presence in Europe.

8

A Culture with Purpose

In conveying our strengths, we believe that equal weight should be given to the human face of XPO. Our company employs over 100,000 extraordinary individuals who have great insights about our customers and our business. The past year was trying at times, but it also brought out the best in Team XPO — our people showed true professionalism by keeping goods moving through supply chains for customers during the pandemic. They know that XPO is 100% committed to their safety.

Our culture is also about being respectful, entrepreneurial, innovative and inclusive. It's about having compassion, being honest and respecting diverse points of view, while operating as a team. We foster emotional safety at work, with robust ethical guidelines that clearly define prohibited behavior, such as harassment, dishonesty, discrimination, workplace violence, bullying, conflicts of interest, insider trading and human trafficking.

In 2020, we created the role of chief diversity officer, and we routinely reinforce the importance of diversity in our culture through open-door management, the XPO University training curriculum, our Workplace virtual community and equal opportunity hiring policies. We also support diverse causes important to our employees, such as Soles4Souls, Girls With Impact, Workfit programs for differently-abled people and the Susan G. Komen Foundation’s fight against breast cancer. We’re proud to be the official transportation partner for the 2021 Susan G. Komen 3-Day Walks®.

Our Pregnancy Care Policy is a gold standard not just for our industry, but for any industry. Any employee of XPO, female or male, who becomes a new parent through birth or adoption can qualify for six weeks of 100% paid leave as the infant's primary caregiver, or two weeks paid leave as the secondary caregiver. In addition, a woman receives up to 20 days of 100% paid prenatal leave for health and wellness and other preparations for her child's arrival.

Our women employees can request pregnancy accommodations without fear of discrimination. This includes "automatic yes" accommodations, such as changes to work schedules and the timing or frequency of breaks, or assistance with certain tasks. More extensive accommodations are easily determined with input from a doctor. Furthermore, we guarantee that a woman will continue to be paid her regular base wage rate while her pregnancy accommodations are in effect, even if her duties need to be adjusted, and she will remain eligible for wage increases while receiving alternate work arrangements.

We’ve also partnered with a leading healthcare network for women and families to offer supplemental health services from over 1,400 practitioners in 20 specialties via a virtual clinic. In total, more than 30 quality benefits are available to XPO women and families in the US. These include fertility services, prenatal and postpartum care, paid family bonding and a return-to-work program.

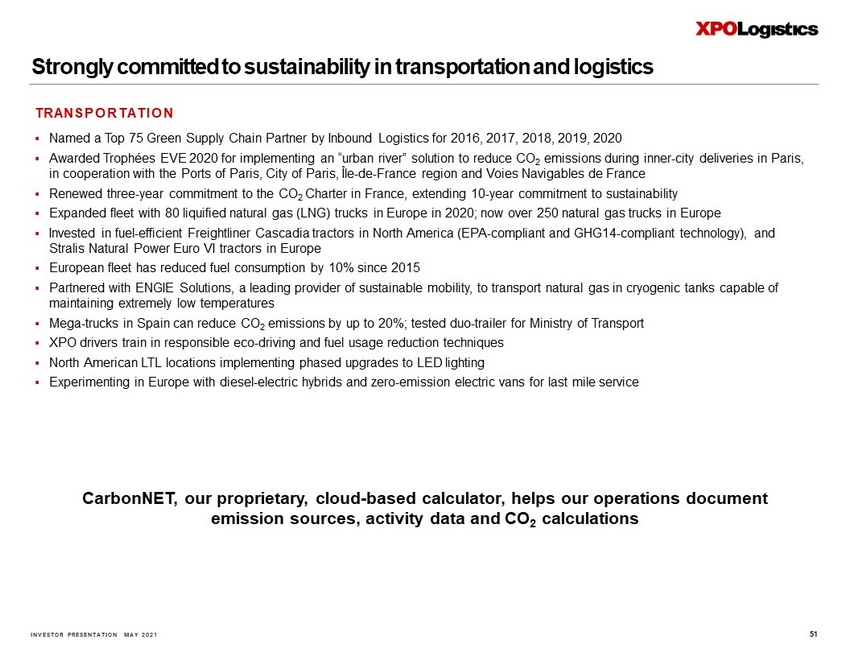

Environmental Sustainability

Environmental sustainability remains a significant priority for us. In the US, XPO has been named a Top 75 Green Supply Chain Partner by Inbound Logistics for five consecutive years. In France, we’ve renewed our commitment to the CO2 Charter for another three years. In Spain, all of our sites meet LEED energy certification standards for 100% consumption of renewable energy.

9

A number of our logistics warehouses are ISO 14001-certified, which ensures environmental and other regulatory compliances. The groundbreaking logistics site we created with Nestlé is operating with environmentally friendly ammonia refrigeration systems, energy-saving lighting, air-source heat pumps for administration areas and rainwater harvesting.

We monitor fuel emissions from forklifts, with protocols in place to take immediate corrective action if needed. Our packaging engineers ensure that the optimal carton size is used for each product slated for distribution, and when feasible, we purchase recycled packaging. As a byproduct of managing returned merchandise, we recycle millions of electronic components and batteries each year.

In our transportation segment, we’ve made substantial investments in fuel-efficient Freightliner Cascadia tractors in North America; these use EPA 2013-compliant and Greenhouse Gas 2014-compliant selective catalytic reduction (SCR) technology. Our North American LTL locations have energy-saving policies in place and are implementing a phased upgrade to LED lighting.

Our modern road fleet in Europe is 98% compliant with Euro V, EEV and Euro VI standards. We also own over 250 natural gas trucks operating in France, the UK, Spain and Portugal, including 80 tractors we purchased in 2020 that use liquified natural gas (LNG). In Spain, we own government-approved mega-trucks to transport freight with fewer trips, and our last mile operations in Europe use electric vehicles for deliveries in certain urban areas, reducing those emissions to zero.

The development of our culture will continue to be a steady march forward, as it has since our founding in 2011. Our Sustainability Report provides details of our global progress in key areas, including safety, employee engagement, diversity and inclusion, ethics and compliance, environmental protection and governance. The latest report can be downloaded from https://sustainability.xpo.com.

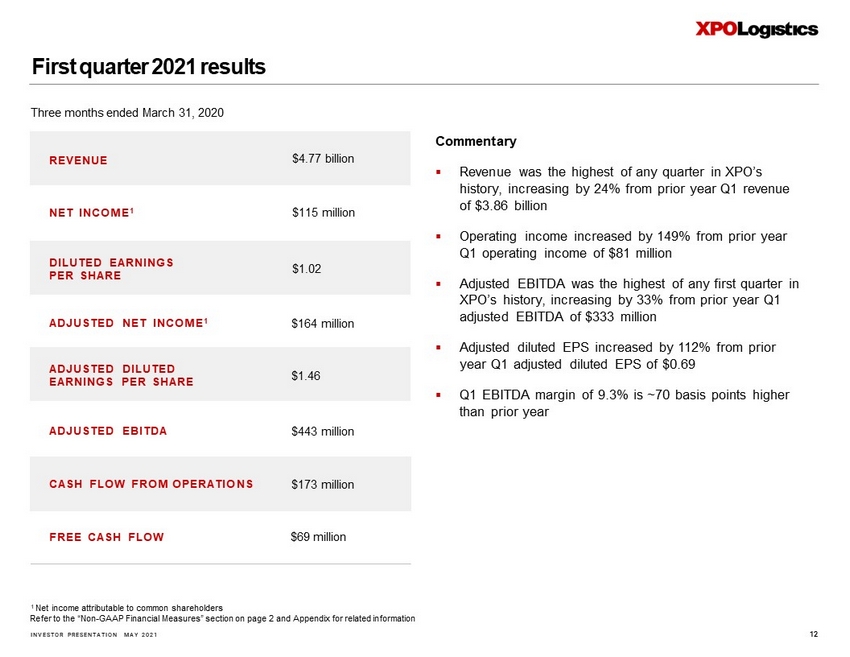

First Quarter 2021 Financial Highlights1

In the first quarter, we reported the highest revenue of any quarter in our history, appreciably outpacing a macro that’s recovering faster than expected. Our net income and adjusted EBITDA were both first quarter records.

Our truck brokerage business is continuing to outperform the market, powered by the growth of our XPO Connect™ digital platform. Our LTL business has strong momentum; industrial demand is rebounding and our technology is continuing to drive margin improvement. In logistics, our record first quarter revenue of $1.82 billion was propelled by the “big three” logistics tailwinds: e-commerce, outsourcing and warehouse automation.

Financial highlights for the quarter are:

| · | $4.77 billion of revenue |

| · | $202 million of operating income |

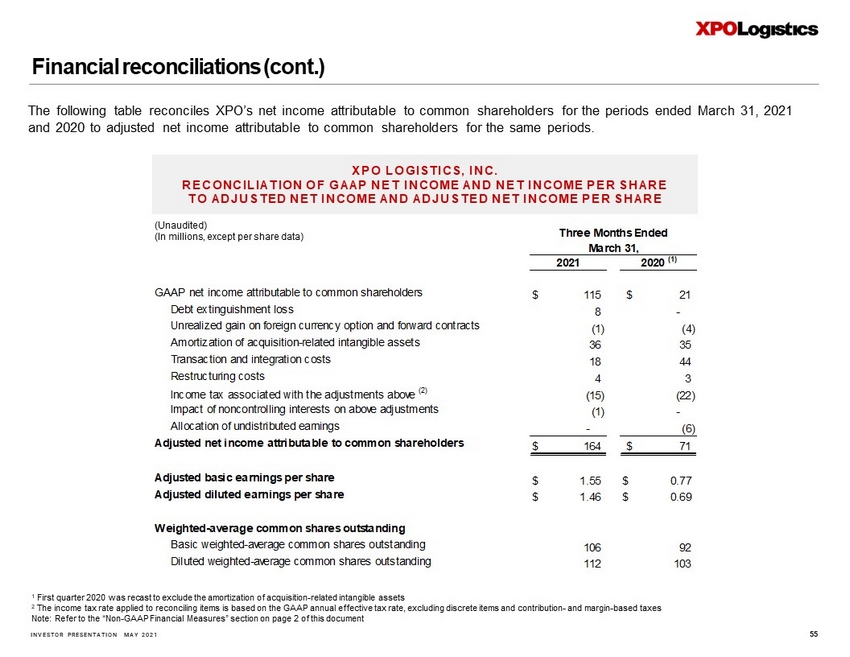

| · | $115 million of net income2 |

1 Reconciliations of non-GAAP financial measures used in this document are provided in the accompanying slide presentation

2 Net income attributable to common shareholders

10

| · | $1.02 diluted earnings per share |

| · | $164 million of adjusted net income2 |

| · | $1.46 adjusted diluted earnings per share |

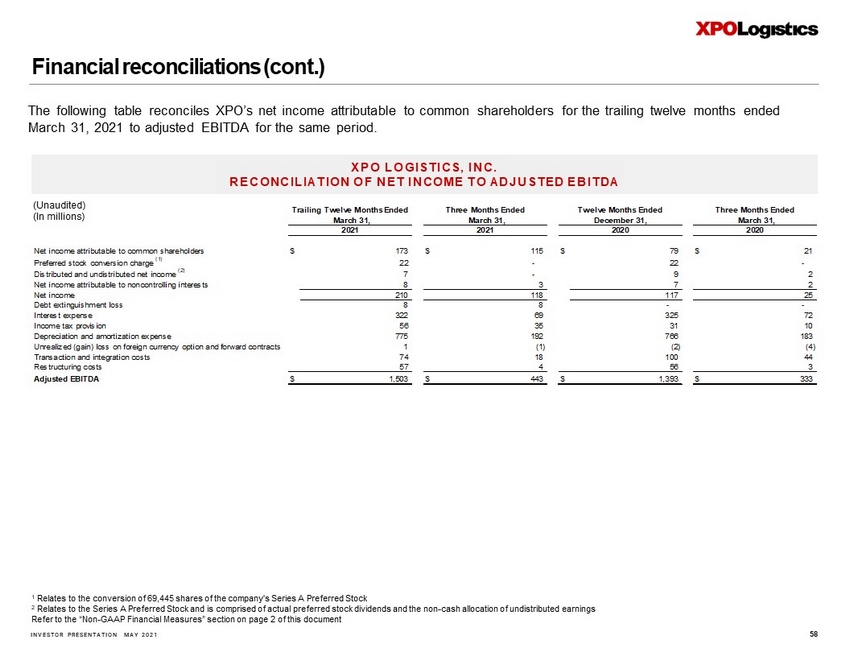

| · | $443 million of adjusted EBITDA |

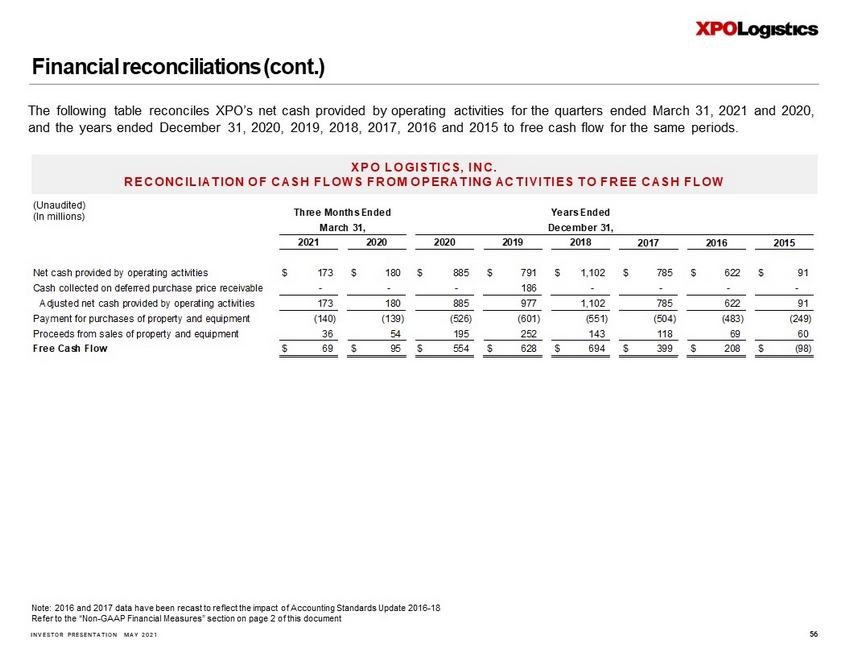

| · | $173 million of cash flow from operations |

| · | $69 million of free cash flow |

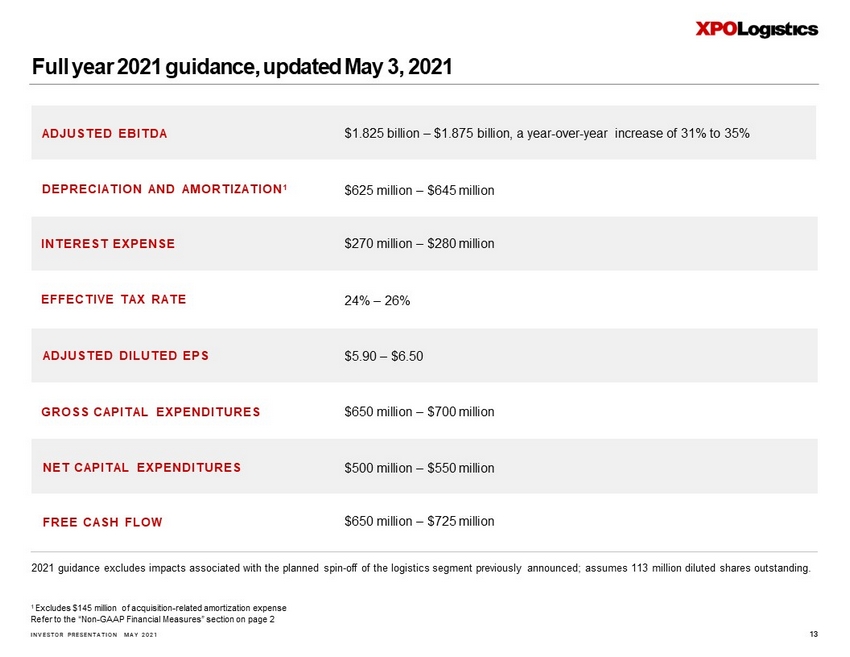

Raises 2022 Guidance

The company issued new full year 2021 targets on May 3, 2021:

| · | Adjusted EBITDA of $1.825 billion to $1.875 billion, compared with the prior guidance of $1.725 billion to $1.8 billion. The new range for adjusted EBITDA reflects a year-over-year increase in adjusted EBITDA of 31% to 35% from 2020, comprised of: |

| – | 28% to 32% growth in adjusted EBITDA in the logistics segment; and |

| – | 30% to 34% growth in adjusted EBITDA in the transportation segment. |

| · | Depreciation and amortization of $625 million to $645 million, excluding $145 million of acquisition-related amortization expense; |

| · | Interest expense of $270 million to $280 million; |

| · | Effective tax rate of 24% to 26%; and |

| · | Adjusted diluted EPS of $5.90 to $6.50, up from the prior range of $5.10 to $5.85. |

With respect to 2021 cash flows, the company issued the following targets:

| · | Gross capital expenditures of $650 million to $700 million, up from the prior range of $625 million to $675 million; |

| · | Net capital expenditures of $500 million to $550 million, up from the prior range of $475 million to $525 million; and |

| · | Free cash flow of $650 million to $725 million, up from the prior range of $600 million to $700 million. |

2021 guidance excludes impacts associated with our planned spin-off of the logistics segment; and assumes 113 million diluted shares outstanding.

Liquidity Position

On March 31, 2021, we had access to approximately $1.7 billion of total liquidity, including $629 million of cash and cash equivalents and $1.1 billion of available borrowing capacity. The company has no significant debt maturing until mid-2023.

In January 2021, we redeemed $1.2 billion of 6.5% Senior Notes due 2022, using available cash, at a price of 100% of the principal amount plus accrued and unpaid interest.

11

Strong Momentum Going Forward

We’re continuing to execute our growth strategy by running the business efficiently, while remaining responsive to changes in our operating environment. This disciplined focus is a major reason why nearly 70% of Fortune 100 companies rely on our services.

When we receive awards for excellence from world-class companies, such as Boeing, Corteva, Diebold, Dow, Ford, GM, Nissan, Nordstrom, Owens Corning, Raytheon, The Home Depot and Whirlpool, we know we’re doing our job.

Our contract with the Tour de France as its official transportation partner has been extended through 2024. This will be the 41st consecutive year we partner with the Tour, and we take great pride in supporting our customer on the world stage. Recently, we were named the official logistics partner for the prestigious IRONMAN triathlons in Europe; our multi-year agreement will commence with our support of more than 20 competitive events this year.

In 2016, we made the Fortune 500 list for the first time, and one year later, XPO was named the fastest-growing transportation company on the list. In 2018, Fortune named us to their Fortune Future 50 list. Gartner has ranked us as a Magic Quadrant 3PL leader for four consecutive years. In Italy, we’ve been awarded Logistics Company of the Year for innovation three times. Logistics Manager named us 3PL of the Year, and both the Netherlands and France ranked us in the top three 3PLs in their respective countries. Forbes ranked us as the top-performing US company on the Global 2000 and one of the best employers in the US.

In February, Fortune named us one of the World's Most Admired Companies for the fourth straight year. And in April, Forbes again named us one of Spain’s best companies to work for. The Financial Times has honored us as a European Diversity Leader, and in 2020, we were named a Winning “W” Company by 2020 Women on Boards for the gender diversity of our board of directors. Newsweek ranked us in the top 100 of America's most responsible companies, and Statista named us one of the most socially responsible companies in France. In the UK, XPO was voted one of Glassdoor’s top three best places to work. We thank our employees for creating the culture that has led to these recognitions.

Now we have the industry’s biggest tailwinds at our back in 2021. Based on a first quarter that solidly beat expectations, and the positive sentiment we hear from our customers, we raised our 2021 guidance for adjusted EBITDA to $1.825 to $1.875 billion, which represents 31% to 35% EBITDA growth year-over-year.

In the near-term, we’ll continue to build our GXO leadership team, following our appointment of eight world-class C-suite executives to date. We’re making excellent progress on the spin-off plan overall, including the filing of our confidential initial Form 10 in March.

There are a lot of reasons to feel bullish about 2021, and we’re off to a very strong start.

Thank you for your interest!

12

Non-GAAP Financial Measures

As required by the rules of the Securities and Exchange Commission (“SEC”), we provide reconciliations of the non-GAAP financial measures contained in this document to the most directly comparable measure under GAAP, which are set forth in the financial tables attached to the accompanying slide presentation.

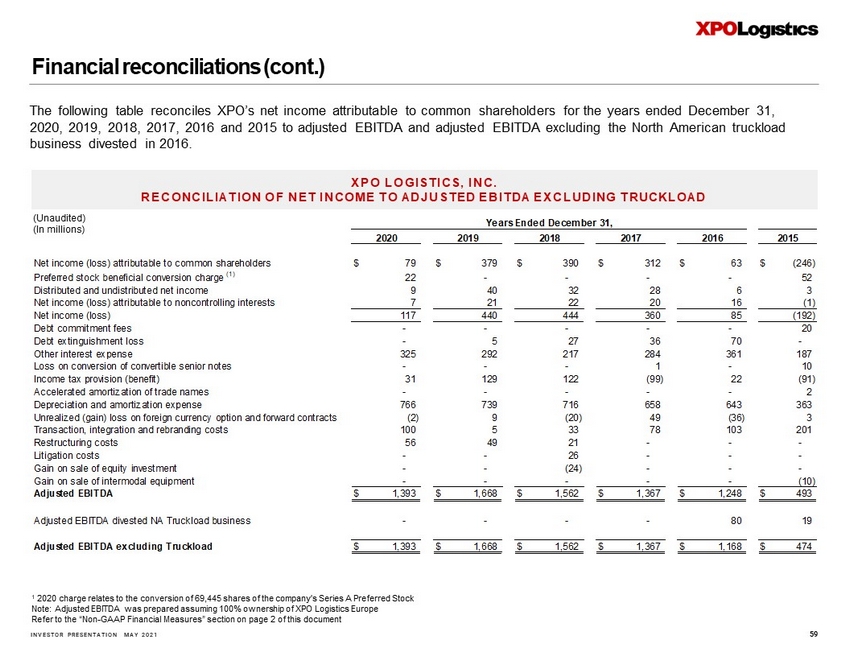

XPO’s non-GAAP financial measures used in this document include: adjusted earnings before interest, taxes, depreciation and amortization (“adjusted EBITDA”) and adjusted EBITDA margin for the three-month periods ended March 31, 2021 and 2020 on a consolidated basis; adjusted EBITDA and adjusted EBITDA excluding truckload for the twelve-month periods ended December 31, 2020, 2019, 2018, 2017, 2016 and 2015; free cash flow for the three-month periods ended March 31, 2021 and 2020, and the twelve-month periods ended December 31, 2020, 2019, 2018, 2017, 2016 and 2015; adjusted net income attributable to common shareholders and adjusted earnings per share (basic and diluted) (“adjusted EPS”) for the three-month periods ended March 31, 2021 and 2020; adjusted EBITDA, adjusted operating income and adjusted operating ratio for our North American less-than-truckload business for the three-month periods ended March 31, 2021 and 2020 and the twelve-month periods ended December 31, 2020, 2019, 2018, 2017, 2016 and 2015; and net debt and net leverage as of March 31, 2021.

We believe that the above adjusted financial measures facilitate analysis of our ongoing business operations because they exclude items that may not be reflective of, or are unrelated to, XPO and its business segments’ core operating performance, and may assist investors with comparisons to prior periods and assessing trends in our underlying businesses. Other companies may calculate these non-GAAP financial measures differently, and therefore our measures may not be comparable to similarly titled measures of other companies. These non-GAAP financial measures should only be used as supplemental measures of our operating performance.

Adjusted EBITDA, adjusted net income attributable to common shareholders and adjusted EPS include adjustments for transaction and integration costs, as well as restructuring costs and other adjustments as set forth in the attached tables. Transaction and integration adjustments are generally incremental costs that result from an actual or planned acquisition, divestiture or spin-off and may include transaction costs, consulting fees, retention awards, and internal salaries and wages (to the extent the individuals are assigned full-time to integration and transformation activities) and certain costs related to integrating and converging IT systems. Restructuring costs primarily relate to severance costs associated with business optimization initiatives. Management uses these non-GAAP financial measures in making financial, operating and planning decisions and evaluating XPO’s and each business segment’s ongoing performance.

We believe that free cash flow is an important measure of our ability to repay maturing debt or fund other uses of capital that we believe will enhance stockholder value. We calculate free cash flow as net cash provided by operating activities, less payment for purchases of property and equipment plus proceeds from sale of property and equipment. We believe that adjusted EBITDA, adjusted EBITDA margin and adjusted EBITDA excluding truckload improve comparability from period to period by removing the impact of our capital structure (interest and financing expenses), asset base (depreciation and amortization), tax impacts and other adjustments as set out in the attached tables that management has determined are not reflective of core operating activities and thereby assist investors with assessing trends in our underlying businesses. We believe that adjusted net income attributable to common shareholders and adjusted EPS improve the comparability of our operating results from period to period by removing the impact of certain costs and gains that management has determined are not reflective of our core operating activities, including amortization of acquisition-related intangible assets. We believe that adjusted operating income and adjusted operating ratio for our North American less-than-truckload business improve the comparability of our operating results from period to period by (i) removing the impact of certain transaction and integration and restructuring costs, as well as amortization expenses and (ii) including the impact of pension income incurred in the reporting period as set out in the attached tables. We believe that net debt and net leverage are important measures of our overall liquidity position and are calculated by removing cash and cash equivalents from our reported total debt and reporting net debt as a ratio of our last twelve-month reported adjusted EBITDA.

13

With respect to our full year 2021 financial targets for adjusted EBITDA, adjusted diluted EPS and free cash flow, a reconciliation of these non-GAAP measures to the corresponding GAAP measures is not available without unreasonable effort due to the variability and complexity of the reconciling items described above that we exclude from these non-GAAP target measures. The variability of these items may have a significant impact on our future GAAP financial results and, as a result, we are unable to prepare the forward-looking statement of income and statement of cash flows prepared in accordance with GAAP that would be required to produce such a reconciliation.

Forward-looking Statements

This document includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, including our future growth prospects for EBITDA in our North American less-than-truckload business, our company's potential profit growth opportunity, our company’s full year 2021 financial targets for adjusted EBITDA, depreciation and amortization (excluding acquisition-related amortization expense), interest expense, effective tax rate, adjusted diluted EPS, gross capital expenditures, net capital expenditures and free cash flow, as well as our company’s planned spin-off of its logistics segment and its plan to pursue an investment-grade credit rating. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. In some cases, forward-looking statements can be identified by the use of forward-looking terms such as “anticipate,” “estimate,” “believe,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict,” “should,” “will,” “expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target,” “trajectory” or the negative of these terms or other comparable terms. However, the absence of these words does not mean that the statements are not forward-looking. These forward-looking statements are based on certain assumptions and analyses made by us in light of our experience and our perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate in the circumstances.

14

These forward-looking statements are subject to known and unknown risks, uncertainties and assumptions that may cause actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. Factors that might cause or contribute to a material difference include the risks discussed in our filings with the SEC and the following: economic conditions generally; the severity, magnitude, duration and aftereffects of the COVID-19 pandemic and government responses to the COVID-19 pandemic; our ability to align our investments in capital assets, including equipment, service centers and warehouses, to our customers’ demands; our ability to implement our cost and revenue initiatives; our ability to successfully integrate and realize anticipated synergies, cost savings and profit improvement opportunities with respect to acquired companies; matters related to our intellectual property rights; fluctuations in currency exchange rates; fuel price and fuel surcharge changes; natural disasters, terrorist attacks or similar incidents; risks and uncertainties regarding the potential timing and expected benefits of the proposed spin-off of our logistics segment, including final approval for the proposed spin-off and the risk that the spin-off may not be completed on the terms or timeline currently contemplated, if at all; the impact of the proposed spin-off on the size and business diversity of our company; the ability of the proposed spin-off to qualify for tax-free treatment for U.S. federal income tax purposes; our ability to develop and implement suitable information technology systems and prevent failures in or breaches of such systems; our substantial indebtedness; our ability to raise debt and equity capital; fluctuations in fixed and floating interest rates; our ability to maintain positive relationships with our network of third-party transportation providers; our ability to attract and retain qualified drivers; labor matters, including our ability to manage our subcontractors, and risks associated with labor disputes at our customers and efforts by labor organizations to organize our employees; litigation, including litigation related to alleged misclassification of independent contractors and securities class actions; risks associated with our self-insured claims; risks associated with defined benefit plans for our current and former employees; and governmental regulation, including trade compliance laws, as well as changes in international trade policies and tax regimes; governmental or political actions, including the United Kingdom’s exit from the European Union; and competition and pricing pressures.

All forward-looking statements set forth in this document are qualified by these cautionary statements and there can be no assurance that the actual results or developments anticipated by us will be realized or, even if substantially realized, that they will have the expected consequences to or effects on us or our business or operations. Forward-looking statements set forth in this document speak only as of the date hereof, and we do not undertake any obligation to update forward-looking statements to reflect subsequent events or circumstances, changes in expectations or the occurrence of unanticipated events, except to the extent required by law.

15

Exhibit 99.2

INVESTOR PRESENTATION MAY 2021 v MAY 2021 Investor Presentation

INVESTOR PRESENTATION MAY 2021 Disclaimers 2 NON - GAAP FINANCIAL MEASURES As required by the rules of the Securities and Exchange Commission ("SEC"), we provide reconciliations of the non - GAAP financial measures contained in this presentation to the most directly comparable measure under GAAP, which are set forth in the financial tables attached to this document . This document contains the following non - GAAP financial measures : adjusted earnings before interest, taxes, depreciation and amortization (“adjusted EBITDA”) and adjusted EBITDA margin for the three - month periods ended March 31 , 2021 and 2020 on a consolidated basis ; adjusted EBITDA and adjusted EBITDA excluding truckload for the twelve - month periods ended December 31 , 2020 , 2019 , 2018 , 2017 , 2016 and 2015 ; free cash flow for the three - month periods ended March 31 , 2021 and 2020 , and the twelve - month periods ended December 31 , 2020 , 2019 , 2018 , 2017 , 2016 and 2015 ; adjusted net income attributable to common shareholders and adjusted earnings per share (basic and diluted) (“adjusted EPS”) for the three - month periods ended March 31 , 2021 and 2020 ; adjusted EBITDA, adjusted operating income and adjusted operating ratio for our North American less - than - truckload business for the three - month periods ended March 31 , 2021 and 2020 and the twelve - month periods ended December 31 , 2020 , 2019 , 2018 , 2017 , 2016 and 2015 ; and net debt and net leverage as of March 31 , 2021 . We believe that the above adjusted financial measures facilitate analysis of our ongoing business operations because they exclude items that may not be reflective of, or are unrelated to, XPO and its business segments' core operating performance, and may assist investors with comparisons to prior periods and assessing trends in our underlying businesses . Other companies may calculate these non - GAAP financial measures differently, and therefore our measures may not be comparable to similarly titled measures of other companies . These non - GAAP financial measures should only be used as supplemental measures of our operating performance . Adjusted EBITDA, adjusted net income attributable to common shareholders and adjusted EPS include adjustments for transaction and integration, as well as restructuring costs and other adjustments as set forth in the attached tables . Transaction and integration adjustments are generally incremental costs that result from an actual or planned acquisition, divestiture or spin - off and may include transaction costs, consulting fees, retention awards, and internal salaries and wages (to the extent the individuals are assigned full - time to integration and transformation activities) and certain costs related to integrating and converging IT systems . Restructuring costs primarily relate to severance costs associated with business optimization initiatives . Management uses these non - GAAP financial measures in making financial, operating and planning decisions and evaluating XPO's and each business segment's ongoing performance . We believe that free cash flow is an important measure of our ability to repay maturing debt or fund other uses of capital that we believe will enhance stockholder value . We calculate free cash flow as net cash provided by operating activities, less payment for purchases of property and equipment plus proceeds from sale of property and equipment . We believe that adjusted EBITDA, adjusted EBITDA margin and adjusted EBITDA excluding truckload improve comparability from period to period by removing the impact of our capital structure (interest and financing expenses), asset base (depreciation and amortization), tax impacts and other adjustments as set out in the attached tables that management has determined are not reflective of core operating activities and thereby assist investors with assessing trends in our underlying businesses . We believe that adjusted net income attributable to common shareholders and adjusted EPS improve the comparability of our operating results from period to period by removing the impact of certain costs and gains that management has determined are not reflective of our core operating activities, including amortization of acquisition - related intangible assets . We believe that adjusted operating income and adjusted operating ratio for our North American less - than - truckload business improve the comparability of our operating results from period to period by ( i ) removing the impact of certain transaction and integration and restructuring costs, as well as amortization expenses ; and (ii) including the impact of pension income incurred in the reporting period as set out in the attached tables . We believe that net debt and net leverage are important measures of our overall liquidity position and are calculated by removing cash and cash equivalents from our reported total debt and reporting net debt as a ratio of our last twelve - month reported adjusted EBITDA . With respect to our full year 2021 financial targets for adjusted EBITDA, adjusted diluted EPS and free cash flow, a reconciliation of these non - GAAP measures to the corresponding GAAP measures is not available without unreasonable effort due to the variability and complexity of the reconciling items described above that we exclude from these non - GAAP target measures . The variability of these items may have a significant impact on our future GAAP financial results and, as a result, we are unable to prepare the forward - looking statement of income and statement of cash flows prepared in accordance with GAAP that would be required to produce such a reconciliation . FORWARD - LOOKING STATEMENTS This document includes forward - looking statements within the meaning of Section 27 A of the Securities Act of 1933 , as amended, and Section 21 E of the Securities Exchange Act of 1934 , as amended, including our future growth prospects for EBITDA in our North American less - than - truckload business, our company's potential profit growth opportunity, our company’s full year 2021 financial targets for adjusted EBITDA, depreciation and amortization (excluding acquisition - related amortization expense), interest expense, effective tax rate, adjusted diluted EPS, gross capital expenditures, net capital expenditures and free cash flow, as well as our company’s planned spin - off of its logistics segment and its plan to pursue an investment - grade credit rating . All statements other than statements of historical fact are, or may be deemed to be, forward - looking statements . In some cases, forward - looking statements can be identified by the use of forward - looking terms such as “anticipate,” “estimate,” “believe,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict,” “should,” “will,” “expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target,” “trajectory” or the negative of these terms or other comparable terms . However, the absence of these words does not mean that the statements are not forward - looking . These forward - looking statements are based on certain assumptions and analyses made by us in light of our experience and our perception of historical trends, current conditions and expected future developments, as well as other factors we believe are appropriate in the circumstances . These forward - looking statements are subject to known and unknown risks, uncertainties and assumptions that may cause actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward - looking statements . Factors that might cause or contribute to a material difference include the risks discussed in our filings with the SEC and the following : economic conditions generally ; the severity, magnitude, duration and aftereffects of the COVID - 19 pandemic and government responses to the COVID - 19 pandemic ; our ability to align our investments in capital assets, including equipment, service centers and warehouses, to our customers' demands ; our ability to implement our cost and revenue initiatives ; our ability to successfully integrate and realize anticipated synergies, cost savings and profit improvement opportunities with respect to acquired companies ; matters related to our intellectual property rights ; fluctuations in currency exchange rates ; fuel price and fuel surcharge changes ; natural disasters, terrorist attacks or similar incidents ; risks and uncertainties regarding the potential timing and expected benefits of the proposed spin - off of our logistics segment, including final approval for the proposed spin - off and the risk that the spin - off may not be completed on the terms or timeline currently contemplated, if at all ; the impact of the proposed spin - off on the size and business diversity of our company ; the ability of the proposed spin - off to qualify for tax - free treatment for U . S . federal income tax purposes ; our ability to develop and implement suitable information technology systems and prevent failures in or breaches of such systems ; our substantial indebtedness ; our ability to raise debt and equity capital ; fluctuations in fixed and floating interest rates ; our ability to maintain positive relationships with our network of third - party transportation providers ; our ability to attract and retain qualified drivers ; labor matters, including our ability to manage our subcontractors, and risks associated with labor disputes at our customers and efforts by labor organizations to organize our employees ; litigation, including litigation related to alleged misclassification of independent contractors and securities class actions ; risks associated with our self - insured claims ; risks associated with defined benefit plans for our current and former employees ; and governmental regulation, including trade compliance laws, as well as changes in international trade policies and tax regimes ; governmental or political actions, including the United Kingdom's exit from the European Union ; and competition and pricing pressures . All forward - looking statements set forth in this deck are qualified by these cautionary statements and there can be no assurance that the actual results or developments anticipated by us will be realized or, even if substantially realized, that they will have the expected consequences to or effects on us or our business or operations . Forward - looking statements set forth in this deck speak only as of the date hereof, and we do not undertake any obligation to update forward - looking statements to reflect subsequent events or circumstances, changes in expectations or the occurrence of unanticipated events, except to the extent required by law .

INVESTOR PRESENTATION MAY 2021 Table of contents 3 KEY FACTORS DRIVING GROWTH AND RETURNS 4 BUSINESS OVERVIEW 5 Q1 2021 KEY FINANCIAL RESULTS 8 GXO: LOGISTICS 14 XPO: TRANSPORTATION 23 SUPPLEMENTAL MATERIALS 39 APPENDIX 53

INVESTOR PRESENTATION MAY 2021 Key factors driving growth and returns 4 Scale positions in large, growing markets ▪ Core markets are large, fragmented and growing, providing multiple opportunities to grow the business organically and through M&A ▪ Market - leading positions across business units, with each strategically benefiting from technology, scale and long - tenured customer relationships Poised to benefit from secular macro tailwinds across all major service lines ▪ Accelerating consumer shift to e - commerce is driving significant gains in both the logistics and transportation businesses ▪ Industrial recovery is turbocharging demand, particularly in our North American LTL business Accelerating momentum in the less - than - truckload business ▪ Largest operating margin improvement in the LTL industry over the last five years; now with the second highest margin in the industry ▪ LTL operational improvements and technology initiatives are expected to drive further growth and margin expansion Best - in - class brokerage platform with digital advantage ▪ Record - setting recent performance, as business continues to execute in a white - hot market; asset - light model converts top - line growth into free cash flow and high ROIC ▪ Proprietary digital brokerage technology is a key strategic advantage in a fast - growing market where shippers are increasingly outsourcing truckload shipments to brokers Major growth drivers are fueling logistics business ▪ COVID has accelerated the growth in e - commerce and the shift to outsourced logistics; both increase demand for our logistics services ▪ Warehouses are becoming increasingly automated for efficiency, speed and safety; we are well - positioned to capitalize on our first - mover advantage as a technology leader in the space Experienced management team with a track record of delivering results ▪ Deep bench of experienced leaders in each business line, with a long history of generating growth, expanding margins and delivering value to shareholders ▪ XPO has beaten consensus estimates for four quarters running, with substantial beats in Q1 2021 and all of H2 2020

INVESTOR PRESENTATION MAY 2021 Business overview

INVESTOR PRESENTATION MAY 2021 Planned spin - off will create two pure - play industry powerhouses 6 Second largest contract logistics provider globally, with one of the largest outsourced e - commerce fulfillment platforms Leading global provider of freight transportation, primarily truck brokerage and less - than - truckload (LTL) services KEY LOGISTICS METRICS 1 KEY TRANSPORTATION METRICS 1 1 As of March 31, 2021 Note: The company expects to complete the spin - off of its logistics segment in the second half of 2021; there can be no assuranc e the spin - off will happen, or of its timing or terms Note: Historical results are not necessarily indicative of the results that may be expected in the future or for the standalo ne businesses after the spin - off ▪ Third largest provider of LTL transportation in North America and a leading LTL network in Western Europe ▪ Second largest truck brokerage provider worldwide ▪ Innovator in digital brokerage transactions, with one of the industry’s most rapidly adopted, fully automated freight management platforms: XPO Connect Œ ▪ Asset - light business characterized by long - term, contractual relationships with high retention rates and low cyclicality ▪ 210 million sq. ft. 1 of warehouse space (99 million sq. ft. in North America; 104 sq. ft. million in Europe; 7 million sq. ft. in Asia) ▪ Innovator in advanced warehouse automation, including robots, cobots , goods - to - person systems and wearables 62% OF 2020 COMPANY REVENUE 38% OF 2020 COMPANY REVENUE TTM revenue $10.7 billion Locations 727 Countries of operation 18 TTM revenue $6.6 billion Warehouses 885 Countries of operation 27

INVESTOR PRESENTATION MAY 2021 ~$ 500 million average annual investment in innovative supply chain technology 7 LOGISTICS ▪ Proprietary warehouse management system manages all distribution processes and warehouse operations ▪ Provides in - house control of robotics and other advanced automation ▪ Integrates transportation and logistics services for retail, e - commerce, omnichannel and manufacturing customers using XPO Direct Œ ▪ Improves productivity in warehouse operations by rightsizing labor resources with XPO Smart Œ analytics LESS - THAN - TRUCKLOAD ▪ Network optimization tools improve LTL linehaul, pickup - and - delivery and routing ▪ Proprietary algorithms with machine learning assimilate constant inflows of data ▪ Visibility facilitates selling LTL across additional verticals ▪ Improves the efficiency of cross - dock operations with XPO Smart Œ analytics TRUCK BROKERAGE ▪ Proprietary XPO Connect Œ marketplace with machine learning drives end - to - end efficiency in brokered freight transactions ▪ Fully automated platform integrates Freight Optimizer capacity management engine ▪ Automates carrier matching to optimal loads ▪ Lowers environmental impact by reducing empty truck miles ▪ Gives carriers access to XPO Connect Œ from their trucks with Drive XPO Œ app KEY TECHNOLOGY BY SERVICE LINE ~1,700 technology professionals focus on continuously improving results

INVESTOR PRESENTATION MAY 2021 Q1 2021 key financial results

INVESTOR PRESENTATION MAY 2021 Industry - leading growth in revenue and adjusted EBITDA 9 REVENUE ADJUSTED EBITDA Note: Both charts exclude the impact of the North American truckload unit divested in October 2016 Refer to the “Non - GAAP Financial Measures” section on page 2 and Appendix for related information 7,533 14,188 15,381 17,279 16,648 16,252 0 4,000 8,000 12,000 16,000 20,000 2015 2016 2017 2018 2019 2020 474 1,168 1,367 1,562 1,668 1,393 0 250 500 750 1,000 1,250 1,500 1,750 2,000 2015 2016 2017 2018 2019 2020 2021F 1,825 – 1,875 $ in millions $ in millions

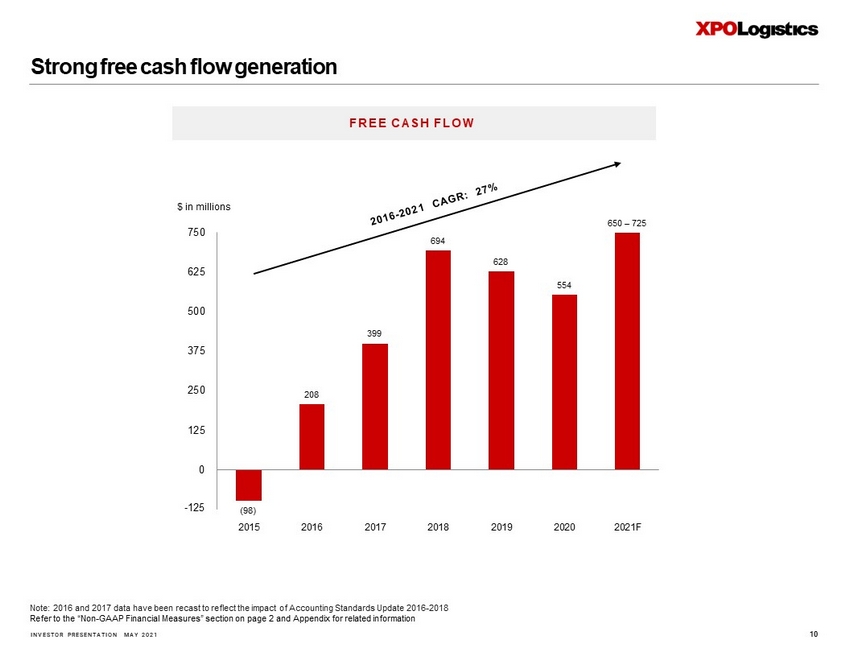

INVESTOR PRESENTATION MAY 2021 Strong free cash flow generation 10 FREE CASH FLOW Note: 2016 and 2017 data have been recast to reflect the impact of Accounting Standards Update 2016 - 2018 Refer to the “Non - GAAP Financial Measures” section on page 2 and Appendix for related information $ in millions (98) 208 399 694 628 554 650 – 725 -125 0 125 250 375 500 625 750 2015 2016 2017 2018 2019 2020 2021F - 125

INVESTOR PRESENTATION MAY 2021 Balance sheet and liquidity as of March 31, 2021 11 NET DEBT 1 $4.6 billion CASH AND CASH EQUIVALENTS $629 million NET LEVERAGE 2 3.1x TOTAL LIQUIDITY $1.7 billion Recent activities ▪ In January, the company redeemed $1.2 billion of 6.5% Senior Notes due 2022 ▪ In March, the company refinanced its $2.0 billion term loan, reducing the interest spread by three - eighths of a point ▪ No significant debt maturities until September 2023 ▪ Substantially all convertible preferred stock converted into common stock in December 2020 1 Calculated as total debt of $5.25 billion less cash and cash equivalents of $629 million 2 Calculated as net debt of $4.6 billion divided by TTM adjusted EBITDA of $1.5 billion Refer to the “Non - GAAP Financial Measures” section on page 2 and Appendix for related information

INVESTOR PRESENTATION MAY 2021 First quarter 2021 results 12 REVENUE $4.77 billion NET INCOME 1 $115 million DILUTED EARNINGS PER SHARE $1.02 ADJUSTED NET INCOME 1 $164 million ADJUSTED DILUTED EARNINGS PER SHARE ADJUSTED EBITDA $443 million CASH FLOW FROM OPERATIONS $173 million FREE CASH FLOW $69 million $1.46 Commentary ▪ Revenue was the highest of any quarter in XPO’s history, increasing by 24% from prior year Q1 revenue of $3.86 billion ▪ Operating income increased by 149% from prior year Q1 operating income of $81 million ▪ Adjusted EBITDA was the highest of any first quarter in XPO’s history, increasing by 33% from prior year Q1 adjusted EBITDA of $333 million ▪ Adjusted diluted EPS increased by 112% from prior year Q1 adjusted diluted EPS of $0.69 ▪ Q1 EBITDA margin of 9.3% is ~70 basis points higher than prior year Three months ended March 31, 2020 1 Net income attributable to common shareholders Refer to the “Non - GAAP Financial Measures” section on page 2 and Appendix for related information

INVESTOR PRESENTATION MAY 2021 2021 guidance excludes impacts associated with the planned spin - off of the logistics segment previously announced; assumes 113 m illion diluted shares outstanding. ADJUSTED EBITDA $1.825 billion – $1.875 billion, a year - over - year increase of 31% to 35% DEPRECIATION AND AMORTIZATION 1 $625 million – $645 million INTEREST EXPENSE $270 million – $280 million EFFECTIVE TAX RATE 24% – 26% GROSS CAPITAL EXPENDITURES $650 million – $700 million ADJUSTED DILUTED EPS $5.90 – $6.50 $650 million – $725 million Full year 2021 guidance, updated May 3, 2021 13 1 Excludes $145 million of acquisition - related amortization expense Refer to the “Non - GAAP Financial Measures” section on page 2 NET CAPITAL EXPENDITURES FREE CASH FLOW $500 million – $550 million

INVESTOR PRESENTATION MAY 2021 GXO: Logistics

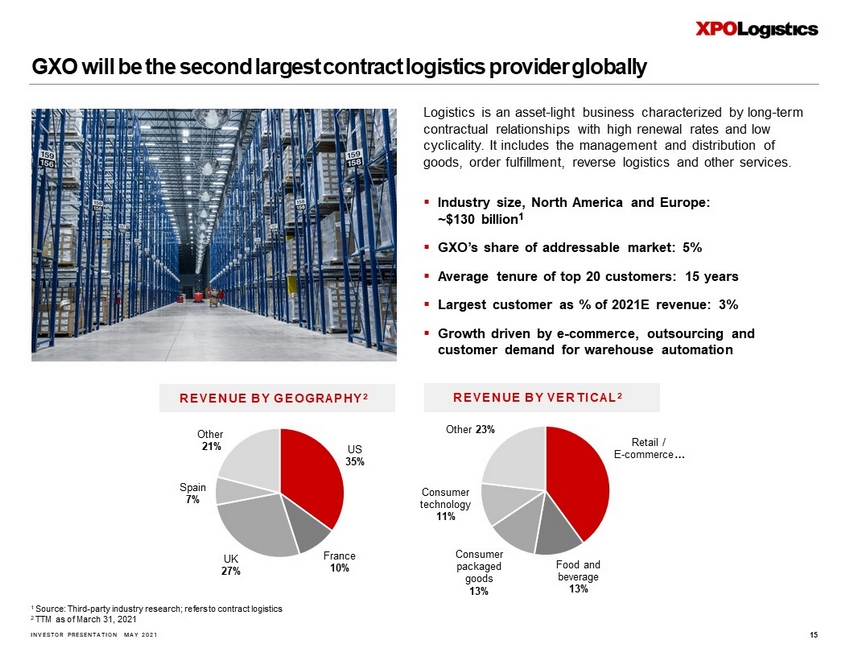

INVESTOR PRESENTATION MAY 2021 US 35% France 10% UK 27% Spain 7% Other 21% Retail / E - commerce … Food and beverage 13% Consumer packaged goods 13% Consumer technology 11% Other 23% GXO will be the second largest contract logistics provider globally Logistics is an asset - light business characterized by long - term contractual relationships with high renewal rates and low cyclicality. It includes the management and distribution of goods, order fulfillment, reverse logistics and other services. ▪ Industry size, North America and Europe: ~ $130 billion 1 ▪ GXO’s share of addressable market: 5% ▪ Average tenure of top 20 customers: 15 years ▪ Largest customer as % of 2021E revenue: 3% ▪ Growth driven by e - commerce, outsourcing and customer demand for warehouse automation REVENUE BY GEOGRAPHY 2 1 Source: Third - party industry research; refers to contract logistics 2 TTM as of March 31, 2021 15 REVENUE BY VERTICAL 2

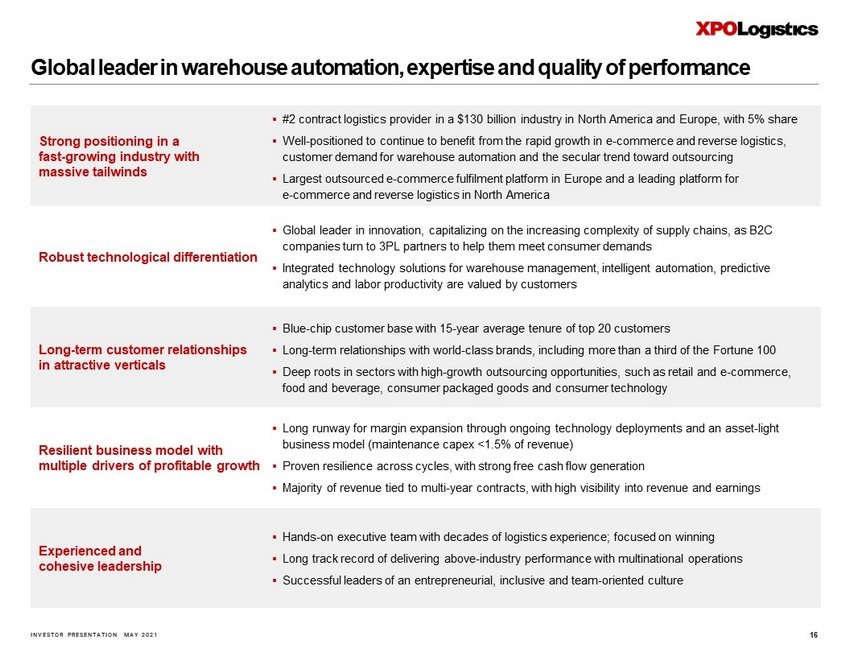

INVESTOR PRESENTATION MAY 2021 Global leader in warehouse automation, expertise and quality of performance 16 Strong positioning in a fast - growing industry with massive tailwinds ▪ #2 contract logistics provider in a $130 billion industry in North America and Europe, with 5% share ▪ Well - positioned to continue to benefit from the rapid growth in e - commerce and reverse logistics, customer demand for warehouse automation and the secular trend toward outsourcing ▪ Largest outsourced e - commerce fulfilment platform in Europe and a leading platform for e - commerce and reverse logistics in North America Robust technological differentiation ▪ Global leader in innovation, capitalizing on the increasing complexity of supply chains, as B2C companies turn to 3PL partners to help them meet consumer demands ▪ Integrated technology solutions for warehouse management, intelligent automation, predictive analytics and labor productivity are valued by customers Long - term customer relationships in attractive verticals ▪ Blue - chip customer base with 15 - year average tenure of top 20 customers ▪ Long - term relationships with world - class brands, including more than a third of the Fortune 100 ▪ Deep roots in sectors with high - growth outsourcing opportunities, such as retail and e - commerce, food and beverage, consumer packaged goods and consumer technology Resilient business model with multiple drivers of profitable growth ▪ Long runway for margin expansion through ongoing technology deployments and an asset - light business model (maintenance capex <1.5% of revenue) ▪ Proven resilience across cycles, with strong free cash flow generation ▪ Majority of revenue tied to multi - year contracts, with high visibility into revenue and earnings Experienced and cohesive leadership ▪ Hands - on executive team with decades of logistics experience; focused on winning ▪ Long track record of delivering above - industry performance with multinational operations ▪ Successful leaders of an entrepreneurial, inclusive and team - oriented culture

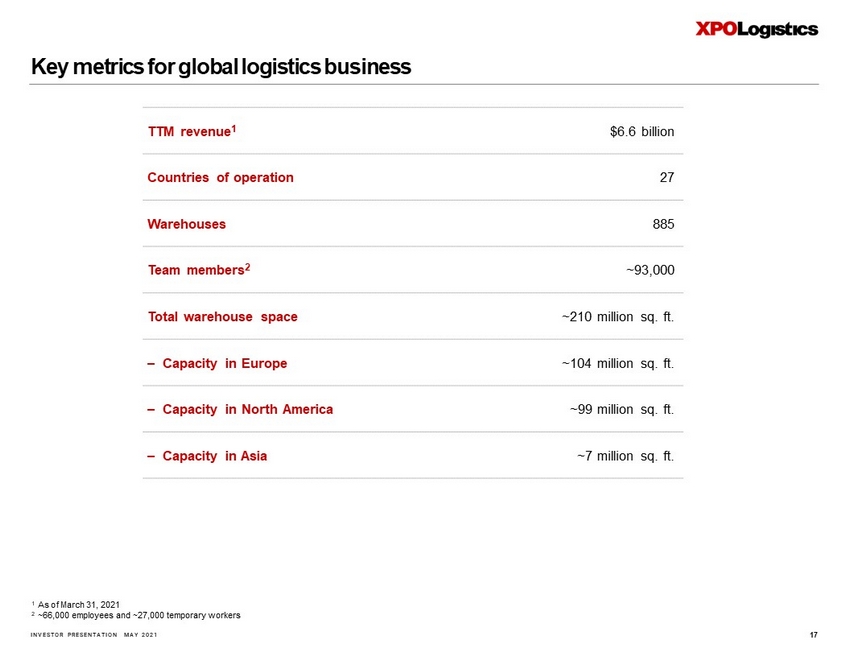

INVESTOR PRESENTATION MAY 2021 TTM revenue 1 $6.6 billion Countries of operation 27 Warehouses 885 Team members 2 ~93,000 Total warehouse space ~ 210 million sq. ft. – Capacity in Europe ~ 104 million sq. ft. – Capacity in North America ~ 99 million sq. ft. – Capacity in Asia ~ 7 million sq. ft. Key metrics for global logistics business 17 1 As of March 31, 2021 2 ~66,000 employees and ~ 27 ,000 temporary workers

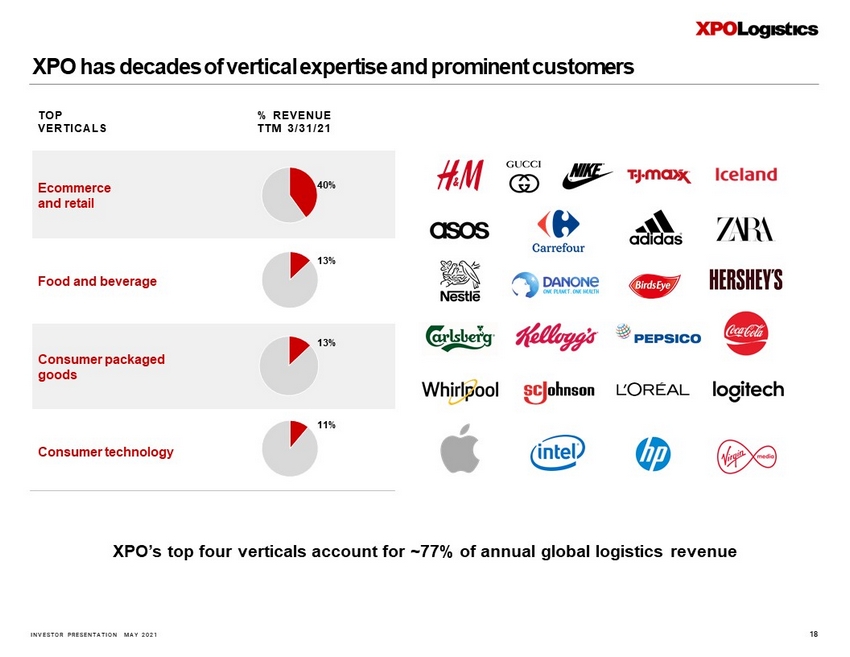

INVESTOR PRESENTATION MAY 2021 XPO has decades of vertical expertise and prominent customers 18 TOP VERTICALS % REVENUE TTM 3/31/21 Ecommerce and retail Food and beverage Consumer packaged goods Consumer technology 11% 13% 13% 40% XPO’s top four verticals account for ~77% of annual global logistics revenue

INVESTOR PRESENTATION MAY 2021 19 Customization positions GXO as a mission - critical partner for customers Differentiated by consistently superior outcomes tailored to customer expectations ▪ Drives significant improvements in labor productivity and throughput ▪ In - house control with warehouse management system facilitates redeployment between projects ▪ Purpose - built solutions optimize warehouse capacity and flexibility ▪ Customizable systems for handling complex product returns solve a fast - growing need for companies faced with burgeoning returns ▪ Full lifecycle management of returned merchandise ▪ Strategic collaboration to help customers achieve ESG goals ▪ C hannel - specific boxing and labeling ▪ Order personalization ▪ Supply chain optimization ▪ Demand forecasting REVERSE LOGISTICS AND AFTERMARKET SUPPORT ADVANCED AUTOMATION AND ROBOTICS HIGH - VALUE - ADD SERVICES

INVESTOR PRESENTATION MAY 2021 20 Intelligent warehouse automation generates measurable improvements ROBOTICS GOODS - TO - PERSON SYSTEMS ADVANCED SORTATION SYSTEMS VISION TECHNOLOGY ▪ Automation delivers reliable, consistent outcomes for customers, with increased speed and accuracy ▪ Warehouse management platform integrates several types of automation as an integrated solution ▪ First - mover advantage with advanced automation; strongly differentiates XPO as logistics partner of choice ▪ Robotics work cooperatively with humans or as standalone solutions ▪ Collaborative robots and autonomous goods - to - person systems overcome space and labor constraints; can move between projects and sites 4 - 6x productivity improvement with employees supported by goods - to - person systems 2x productivity improvement with employees who work alongside cobots

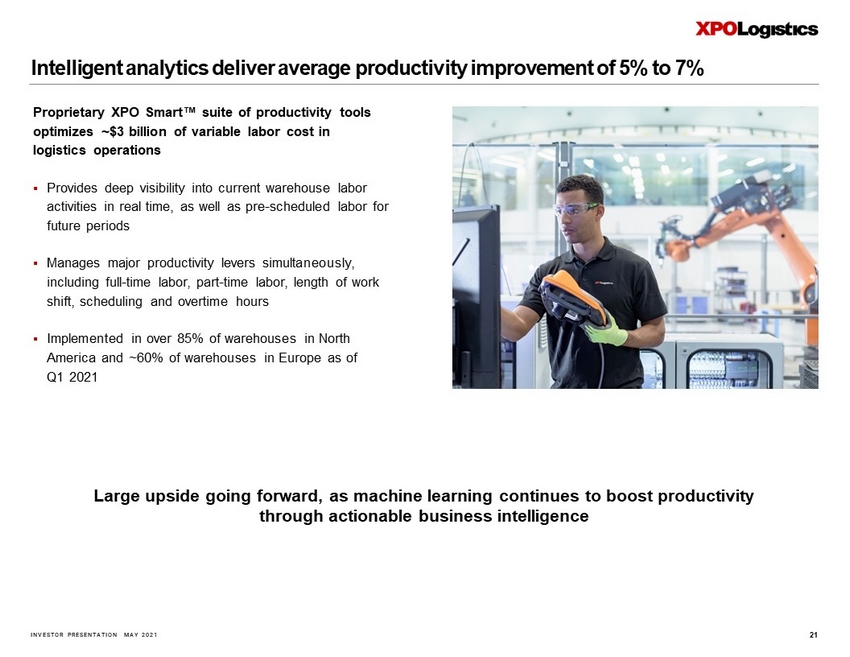

INVESTOR PRESENTATION MAY 2021 21 Proprietary XPO Smart Œ suite of productivity tools optimizes ~$3 billion of variable labor cost in logistics operations ▪ Provides deep visibility into current warehouse labor activities in real time, as well as pre - scheduled labor for future periods ▪ Manages major productivity levers simultaneously, including full - time labor, part - time labor, length of work shift, scheduling and overtime hours ▪ Implemented in over 85% of warehouses in North America and ~60 % of warehouses in Europe as of Q1 2021 Large upside going forward, as machine learning continues to boost productivity through actionable business intelligence Intelligent analytics deliver average productivity improvement of 5% to 7%